Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus

US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  Chip Stocks Rally as Samsung and SK Hynix’s $1.3 Trillion Investment Plan Boosts AI Optimism

Chip Stocks Rally as Samsung and SK Hynix’s $1.3 Trillion Investment Plan Boosts AI Optimism  U.S. Stocks End Q2 Higher as Strong Jobs Data and AI Rally Lift Wall Street

U.S. Stocks End Q2 Higher as Strong Jobs Data and AI Rally Lift Wall Street  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

'Impossible Trinity/Trilemma' is an economic concept which suggests that a country can’t all the three following at the same time; a fixed foreign exchange rate, free capital movement, and an independent monetary policy. And the ‘Trinity’ is back to haunt China again and this time around it has more firepower.

Why we say, ‘firepower’?

Simply because, this is not the first time China has faced the challenges of the impossible trinity and every time the country’s central bank (People’s Bank of China) has cleverly maneuvered its policy to avert the ‘Trinity’ disaster, which usually gets triggered by sudden explosion of volatility with either peg break or rise in the interest rates. However, every time, as China continued growing at a rapid pace, countering the Trinity under modernization and fixed exchange rate regime became difficult.

Brief history:

Due to these increasing challenges and to modernize its financial system, China de-pegged its currency from the U.S. dollar back in 2005 and since then it has gradually opened its economy to the world and reduced control over the capital account. However, PBoC still controls the volatility of the USD/CNY exchange rate by announcing a central point and the exchange rate is allowed to move within 2 percent band

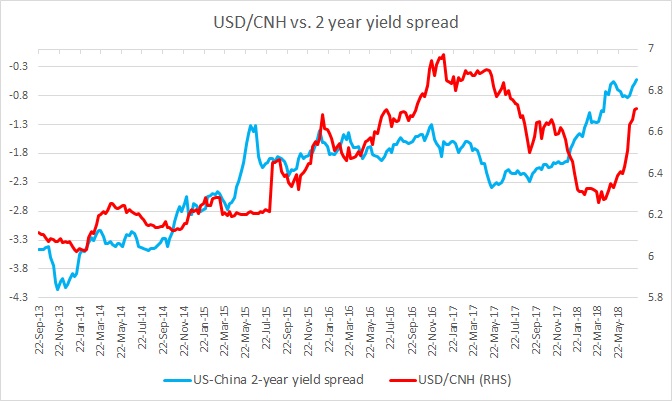

In modern day’s China counters the trinity using its vast foreign exchange reserve from time to time but recent history suggest that it is becoming increasingly difficult for the $11-12 trillion economy to counter the ‘Trinity’. In the above chart, look around March-August 2015 area, and you would see from the exchange rate movement that it was managed by PBoC, whereas the rate differential between the U.S. and China moved sharply in favor of the USD. After refusing to let the Yuan depreciate for several months, PBoC finally had to announce a one-time devaluation of the Yuan, leading to the biggest intraday selloff in the stock markets around the world.

Since the event, PBoC has further reduced its intervention in the foreign exchange market for a prolonged period.

The challenge now:

The figure above clearly suggests that the interest rate spread between China and the U.S. govt. bonds are in decline with the United States firing its all engines of growth and the U.S. Federal Reserve raising interest rates in response to a growing economy with the higher inflation rate.

It is happening at a time when the current U.S. administration has waged a war against China’s massive goods’ trade surplus with the United States, which reached $375 billion in 2017.

With the U.S. rates likely to increase further, the PBoC would either have to let the domestic interest rates rise, or let the yuan to depreciate based on market expectations.

We don’t expect the central bank, which has cleverly countered the trilemma over the decades to move aggressively and challenge. FxWirePro’s money is on letting the exchange rate depreciate as it would automatically counter some impacts of tariffs.