Kentucky School District Secures $27 Million in Social Media Addiction Lawsuit Settlements

Kentucky School District Secures $27 Million in Social Media Addiction Lawsuit Settlements  Ether Breaks Below $2,100: Triple EMA “Sell-the-Rally” Setup Targets $1,900

Ether Breaks Below $2,100: Triple EMA “Sell-the-Rally” Setup Targets $1,900  ETH Cracks $2,100 in Bitcoin’s Wake as Bearish EMA Stack Deepens; Sellers Target $1,900 on Rallies

ETH Cracks $2,100 in Bitcoin’s Wake as Bearish EMA Stack Deepens; Sellers Target $1,900 on Rallies  HP Q2 2026 Earnings Beat Expectations Despite Memory Chip Pressure

HP Q2 2026 Earnings Beat Expectations Despite Memory Chip Pressure  Samsung Union Dispute Escalates Over Semiconductor Bonus Vote

Samsung Union Dispute Escalates Over Semiconductor Bonus Vote  Xiaomi Shares Drop After Weak Q1 Earnings Amid Rising Smartphone Costs

Xiaomi Shares Drop After Weak Q1 Earnings Amid Rising Smartphone Costs  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  Blue Origin New Glenn Rocket Explodes During Launch Pad Test, Delaying Space Ambitions

Blue Origin New Glenn Rocket Explodes During Launch Pad Test, Delaying Space Ambitions  SpaceX IPO Could Become Largest in History with $1.8 Trillion Valuation Target

SpaceX IPO Could Become Largest in History with $1.8 Trillion Valuation Target  Salesforce Q1 FY2027 Earnings Beat Expectations Despite Soft Q2 Revenue Outlook

Salesforce Q1 FY2027 Earnings Beat Expectations Despite Soft Q2 Revenue Outlook  SoftBank to Invest €75 Billion in France AI Data Center Expansion by 2031

SoftBank to Invest €75 Billion in France AI Data Center Expansion by 2031  Meta AI Push Could Add $26 Billion in Revenue by 2027, Wolfe Research Says

Meta AI Push Could Add $26 Billion in Revenue by 2027, Wolfe Research Says

In a bid to play catch up with technology companies and younger generations of consumers, central banks are finally starting to take digital currencies seriously. Countries such as Sweden, China, and India have establish pilot digital currencies – respectively, the e-krona, e-yuan and e-rupee – via their central banks. In the finance sector, these are known as central bank digital currencies (CBDCs).

The purpose, scale and status of such efforts vary considerably. In Sweden, the goal is to investigate the potential transition from banknotes to a digital currency, and the e-krona remains in the starting blocks. In China, the “digital renminbi” started to roll out in 2020, and its goal is to allow the state to better control the retail economy. India launched an e-rupee pilot in 2022 and its purpose is to facilitate a broad range of transactions. Meanwhile, the United States is exploring the potential repercussions of establishing its own digital currency.

Along the same lines, the European Union is currently toying with the idea of launching its own digital currency, the e-euro. As the European Central Bank (ECB) explains, it would provide a digital alternative to existing payment methods with the goal of increasing the security and stability of the EU’s monetary system. The e-euro would be held in digital wallets, with transactions facilitated by the use of blockchain.

A crucial difference between the e-euro (a CBDC) and cryptocurrencies is that its overall quantity – the number in circulation – would not be capped. Because bitcoins and other cryptocurrencies aren’t issued by central banks, the number in circulation is limited by the fact that creating new ones requires “mining”, an energy-intensive process that involves solving extremely complicated math problems. Not the case with the e-euro, as it would be regulated by the European Central Bank and be linked directly to the euro itself – there will be no exchange rate, it would simply be the euro in another format.

While there is a superficial similarity between the e-euro and “stablecoins” – cryptocurrencies whose value is pegged to a major currency – the e-euro would be issued and controlled from a public entity. This will ensure stability in valuations and regulation.

The case in favour

The 1 million euro question is why is the ECB would consider a digital currency. While we all have a centuries-long familiarity with physical currencies, digital ones have some advantages:

-

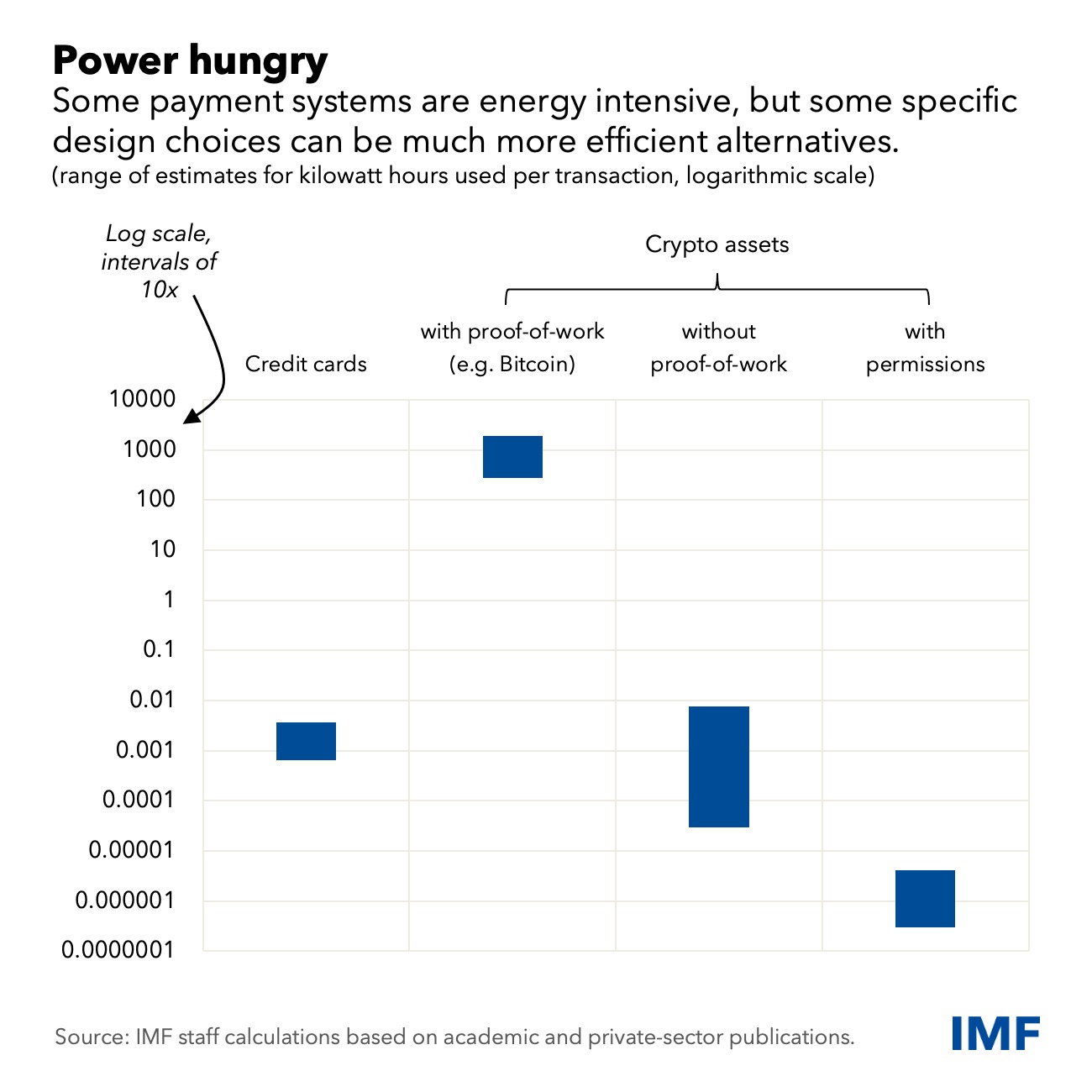

Less resource intensive. A central bank digital currency doesn’t require printing, validation, circulation, monitoring and replacement, and thus would have a considerably lower ecological footprint. That it will be issued rather than mined adds to its energy efficiency. The International Monetary Fund estimates that a CBDC’s payment system for clearance and settlement could use hundreds of thousand of times less energy than physical currencies and cryptocurrencies while maintaining low transaction costs.

-

Increased banking access. Because a digital euro would be directly managed by central banks, it would eliminate the need for intermediaries such as private financial institutions. It thus has the potential to reduce economic exclusion, such as in the cases of “the unbanked” – low-income people without bank accounts. The ECB would create and sustain the required infrastructure, making the e-euro available to all. For example, while private institutions would require a minimum credibility score to open an account, governments could facilitate access to money by opening digital wallets as part of a social policy agenda.

-

Economic sovereignty. It can protect the euro from competing CBDC and other cryptocurrencies and thus defend Europe’s economic sovereignty. It will also allow governments to monitor transactions and so reduce tax avoidance and money laundering .

Where a digital currency leaves central and commercial banks

Given the potential advantages of central bank digital currencies, what is holding countries back? Everything depends on how CBDCs are be designed and implemented, and some challenges that might overshadow any potential.

-

Pushing back against private digital currencies. Imagine a world where private digital currencies like bitcoin or Facebook’s libra become the means for a substantial share of world’s financial transactions. In this world, the value of the means of exchange would be entirely determined by supply and demand or by the private venture – for example, Facebook itself. The introduction of CBDCs would enable central banks to determine the value of money itself and thus help ensure their country’s monetary sovereignty. People will still be able to choose between national currencies or those supported by private firms, but with the e-euro, Europe will at least be on an equal footing.

-

Balancing security and privacy The basic principle of tangible money is anonymity. In its cash format, money can be exchanged for goods or services without necessarily disclosing one’s identity with every transaction. A fully secure digital currency would require that all transaction information be reported to the authorities, while a fully private one disclose no information. The former would give too much power to central authorities, while the latter would encourage tax avoidance and other nefarious behaviour. The traceability of blockchain can assist in tracking back the full financial history, but should the identity of the actor be public information? The e-euro is likely to operate in a semi-anonymous format to preserve a balance between security and privacy.

-

More stability, less speculation. The initial idea of digital currencies was that they would become decentralized means of exchange, governed by the forces of supply and demand. However, they shortly became speculative assets, subject to vertiginous spikes and brutal crashes. Instead, a major currency should reflect the conditions of the real economy rather than speculation about its future state.

So is the e-euro something that we need or want? This depends on how it will be designed and regulated. For this particular venture, given the complexity of EU regulation, the devil is in the details.

{kind=link}