Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

AUDUSD medium-term perspectives: The ongoing structural Chinese slowdown is expected to remain orderly, which should provide reasonable support to Australia’s commodity exports. Our commodity strategists see iron ore prices supported above $60/t in 2018, but coking coal prices to decline. There are thus downside risks to the AUD from these factors.

Over the course of Q1’18, we look for AUDUSD to return to the 0.75 area seen in early Dec 2017. This should occur if interest rate markets move closer to Westpac’s view of no change in the RBA cash rate this year and if the prospect of increased supply cools the recent commodity price rally. But a firmer US dollar is probably necessary to get as far as 0.75.

AUD is a strong USD-hedge candidate since one-touch AUD put pricing benefits from wafer thin forward points and risk-reversals that renders negative carry of AUD selling almost negligible, and the underlying itself provides fundamental diversification for the broad reflation theme given Australia’s unique domestic headwinds, as well as useful equity beta should the breakneck rally in stocks hit a roadblock.

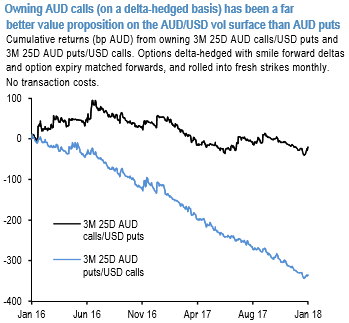

That AUD is worth selling via options does not necessarily imply we find AUD risk-reversals “cheap” enough to warrant owning vanilla AUD puts outright – indeed, recent spot-vol correlation in AUDUSD has been sharply positive (spot up, vol up) in defiance of the persistent bid for AUD puts on riskies, indicating much better value in owning AUD calls rather than puts on the surface (refer above chart).

In light of this, the reduced risk-reversal sensitivity of one-touches is preferable to vanillas while still retaining healthy mark-to-market P/L sensitivity to spot moves. Off spot ref. 0.8035, consider 2M 0.77 strike AUD put/USD call one-touches for 20.7% indicatively.