Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

In mid-August, the Mexican central bank somewhat surprisingly for many lowered its key interest rate. The accompanying statement contained no indications as to how monetary policy would continue. The minutes of the meeting show that the central bankers agree that there are downside risks with regard to the economy.

On the other hand, there is no agreement on inflation risks. The forecast uncertainty is regarded as quite high. Not everyone sees the risk for inflation as pointing downwards. In addition, the central bank expressed surprise that inflation expectations have remained stable and have not declined in line with the weak economy and declining inflation rates.

In this context, the focus is on today's inflation data release for the month of August. If this continues to weaken, this would argue for a further rate cut this month.

However, if it surprises significantly upwards, the sceptics in the board could gain the upper hand. External factors are currently dominating the Mexican peso. But if the central bank becomes increasingly dovish, the peso is likely to become more susceptible to risk-off phases.

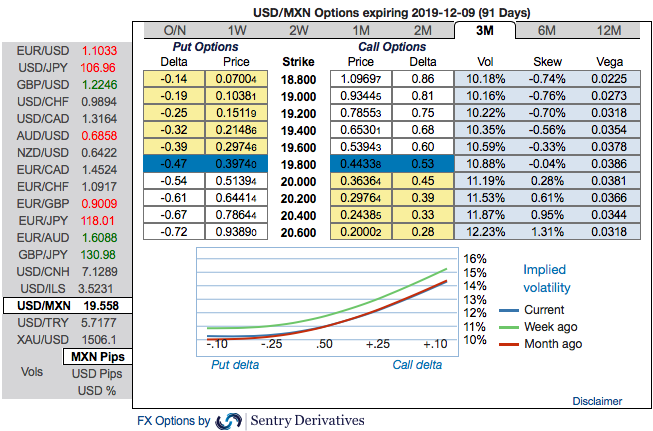

Technically, USDMXN major uptrend remains intact despite some minor corrections (refer above technical chart). We maintain MXN projections of 22 for the end- 2019 and our long USD recommendations in options. The peso’s high carry is likely the reason for MXN’s outperformance this year among EMFX peers. Yet, extended MXN longs positions, BoP weakness, political uncertainty and some fiscal deterioration in our view make MXN more likely to weaken for the rest of the year.

Of late, MXN seemed to be extending recovery threatening upper bound of the recent range.

But please be noted that the 3m USDMXN implied volatility skews signal continued upside risks. The previous massive sell-off of Mexican peso caused a vol surface dislocation, nudging skews to the highest since the 2016 US Presidential elections. Delta hedged 1*1.5 ratio call spreads exploit the dislocation while also having historically offered a superb performance. +1Y/-3M calendars of risk reversals take advantage of the lagging back-end vs front-end implied skews, spot reference: 19.50 levels. Courtesy: Commerzbank, Sentry & Tradingview.com