Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

It is generally assumed that the Bank of England will once again raise the upper limit of its asset purchases today. Considering the speed at which it is currently purchasing assets it would have reached the existing limit within weeks. An increase by approx. GBP 100bn would be sufficient to keep up purchases at the current rate at least until the next meeting in August. At the last meeting two MPC members had already voted in favour of raising the limit by this amount, which is why the market is even talking this sum. It is quite trivial: if the MPC decides on a higher amount, that would be a dovish signal, as the BoE would commit to continued asset purchases past the next meeting rather than waiting until then to take a decision. Sterling would come under pressure as a result; however not just because of the purchases in themselves, but also because that in particular would signal that the BoE prefers to do a little too much rather than a little too less. And that in turn might fuel speculation about negative interest rates.

More recently, rate expectations had risen again on the market, no doubt also as a result of a more optimistic economic outlook. However, the risk is high that the BoE will dampen these expectations by providing a rather dovish outlook, as the Fed did last week.

Brexit is being overshadowed, this is only temporary and GBP remains vulnerable from a great sense of realism amongst investors about the government's objectives for the EU trade talks and its credible threat still to walk away in the pursuit of regulatory autonomy from the EU and freedom from strict level playing field commitments. As a result of the Brexit-virus one-two we are lowering the GBP forecast.

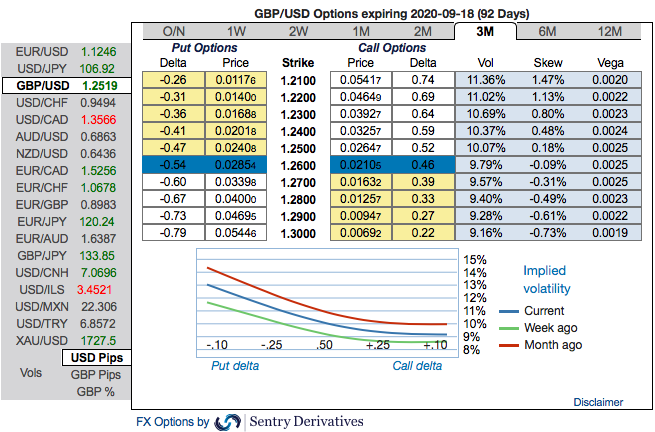

Options Strategy (Debit Put Spread): Contemplating above factors, wise to deploy diagonal options strategy by adding short sterling: Stay short a 2M/2W GBPUSD put spread (1.2650/1.14), spot reference: 1.2435 level.

The Rationale: Observe the 3m GBP’s positive skewness that has stretched towards OTM Put strikes upto 1.21 levels, hence, options traders are expecting that the underlying spot FX to slide southwards.

To substantiate the downside risk sentiment, risk reversal numbers have still been signalling bearish hedging sentiments in the long run. One can observe fresh negative bids that indicates hedgers have shown renewed interests for bearish risks in the months to come.

Hence, we advocate the diagonal options strategy on both hedging and trading grounds. Courtesy: Sentry, Saxo & Commerzbank