New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?

The RBA outlook (on hold for some time) is anchoring front end valuations. We expect 3yr swap rates to remain in a 1.8% to 2.3% range, with core inflation still below 2%.

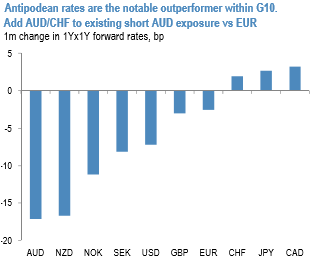

While AUD money markets rates have rallied by more than any other G10 currency over the past month (refer above chart). In the process, the front-end of the curve has inverted again as rate cuts have started to be priced again (roughly 10bp is now priced in – refer above chart). The RBA is unlikely to offer any additional encouragement for rate bulls or AUD bears at next week’s policy meeting as we expect it to stick to its broadly neutral tone of recent months.

Nevertheless, we believe negative momentum in AUD is durable as this is being driven by a confluence of fundamental forces that are both diverse as well as persistent, namely evidence of a downturn in the domestic credit cycle that is manifesting itself in weaker housing market indicators and the performance of bank stocks, together with external factors including the ongoing slide in metals prices and the continued reservations about the Chinese growth cycle (the two are obviously in part inter-related). European currencies are on the other side of the cyclical divide and while growth expectations are no longer being upgraded as powerfully as they were, the delivery of strong growth in the region should sustain an ongoing upgrade in what remain structurally cheap currencies.

We see no reason not to include CHF in this category of undervalued currencies. We accept that this assessment is controversial but in support of this we merely cite the massive intervention the SNB has needed to undertake to prevent a more aggressive appreciation in the currency. Intervention this year is running at twice the pace of last year and nearly 70% greater than the current account surplus. Official intervention may constitute a prior evidence of a currency undervaluation, but at the same time, of course, it also implies the currency is not free to appreciate so long as the SNB continues to sell.

What consequently is significant for CHF, and why we are increasing CHF exposure, is evidence that the SNB is finally tapering its intervention activities following the safe passage of the French election (what possible pretext would it have to intervene now that political risk has abated?).

Average intervention over the past two weeks has dropped to only CHF 0.5bn. This is the slowest rate of intervention since last December and barely a fifth of the peak rate of intervention around the French election (refer above chart). The official door for CHF appreciation seems ajar.

Sell AUDCHF at 0.7170with a stop at 0.7320.

Stay long EURAUD from 1.4840 May 5th. Marked at +1.96%. Raised stop to 1.50.

Sold USDCHF at 0.9782 on May 18. Marked at +1.48%. Lowered stop to 0.9750.