Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

We reckon that the European economy was too fragile for the euro to be able to capitalize on the abrupt change in tone from the Fed or the threat to the credibility of US policymaking.

This stance hasn’t necessarily altered in the intervening period, even though the Fed has now gone even further in signaling not only a shift in stance but also potentially a change to its reaction function, one that is more permissive of an inflation overshoot. Crucially for EURUSD, the European data flow remains distinctly poor, Italy, for instance, is languishing in a self-inflicted recession, and the ECB is now acknowledging the persistence of these downside forces in a way that suggests it could temper its forward guidance on rates, potentially as soon as the March ECB meeting when the staff forecasts are next updated.

Whereas it was understandable that EURUSD popped higher on the Fed, it is also understandable that the euro has been unable to sustain, let alone build on, those advances.

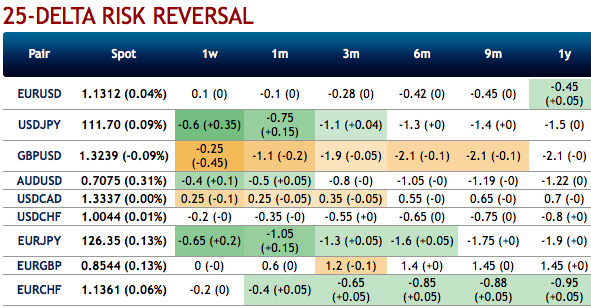

EURUSD OTC outlook:

Please be noted that EURUSD shows convergence between implied volatility (IV) and historic volatility (HV) curves, the trend of lower vols is still imminent. Also, be noted that spot and risk reversal curves. Volatility traders perceptibly expect only about what is likely to and what actually turns out. As you could observe the above chart, Jan’2018 seems to be an average month as the divergence between implied volatility and historic volatility. IVs have constantly been sliding, while RVs are also following.

While spot curves move in tandem with the risk reversal curve until of-late, now they are also showing convergence.

We could foresee potential for further USD strength and limited risk of significant USD weakening this year, and notably, our EURUSD forecast is now running close to forwards on all horizons (vs previously above) and across tenors.

As a result, we recommend hedging USD-denominated income via risk reversals: this allows one to profit from some dollar strength near term (as per our call), yet still secures a worst-case rate without locking in the negative carry from the outset.

From this perspective, the real far-off month, when HV is actually lower than implied volatility, then the only such instance of convergence during the recent timeframe observed. While 3m positively skewed IVs have stretched on either side to signal both upside and downside risks. Skews stretched towards both OTM calls and OTM put strikes signifies hedgers interest on either side.

Overall, the topic is particularly relevant at a time when EURUSD forward points are at a historic all-time high and IVs are dipping, that increases the interest of looking for derivatives-based strategies for hedging long USD cash positions. Courtesy: JPM & Danske

Currency Strength Index: FxWirePro's hourly EUR is flashing at 70 (bullish), hourly USD spot index is sliding towards -96 levels (which is bearish), while articulating (at 07:18 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex