Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

A few more central banks tiptoe to the exit 2017 was the year in which more central banks broke ranks. We expect this to continue in 2018. The Fed will hike four times and the BoC two, which supports long positions in USD and CAD.

EUR should benefit from the prospect of the ECB completing QE just as it rallied on the expectation of tapering this year.

We pair EUR vs NZD to neutralize the risk to EURUSD from a further repricing of the Fed. The RBNZ is an unlikely candidate to signal tighter policy as the slowdown in migration intensifies the downturn in housing and argues against a policy response to upside inflation risks from minimum wage increase etc. The 3m window KO halves the premium compared to a digital call.

In Sweden, the prospects of a policy pivot were delayed not derailed this year. EURSEK is currently overshooting cyclicals by over 4% the most since 2010. The rebound in inflation to 2.0% in November reduces the risk of the central bank extending QE again next week (this was 0.3% ppt higher than the Riksbank's estimate), although it could still push back the lift-off point for rates by a quarter to 3Q18 in order to better align itself with the ECB’s extension of QE through September.

Long a 9-mo 1.80 EURNZD digital call with a 3m 1.80 window KO. Paid 17.5% on November 21. Marked at 19.04%.

Long a 6m 9.60 EUR put/SEK call. Paid 57.2bp November 21. Revalued at 52bp.

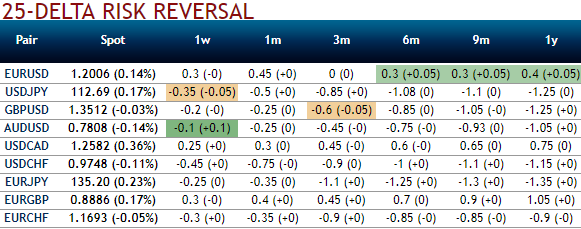

We advocate deploying shorts in futures contracts of near-month tenors with a view to arresting further potential bearish risks of USDCAD, alternatively, we advocate buying USDCAD 3m risk reversal strikes 1.3440/1.2450 (at spot ref: 1.2068).