Goldman Sachs Sees U.S. Dollar Holding Firm as Strong Economic Data Supports Outlook

Goldman Sachs Sees U.S. Dollar Holding Firm as Strong Economic Data Supports Outlook  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  J.P. Morgan Sees Major Upside for Prysmian as Optical Fiber Prices Surge

J.P. Morgan Sees Major Upside for Prysmian as Optical Fiber Prices Surge  Gold Cracks $4,500: Iran-Fed Double Whammy Sends Bullion into Bearish Freefall Toward $4,000

Gold Cracks $4,500: Iran-Fed Double Whammy Sends Bullion into Bearish Freefall Toward $4,000

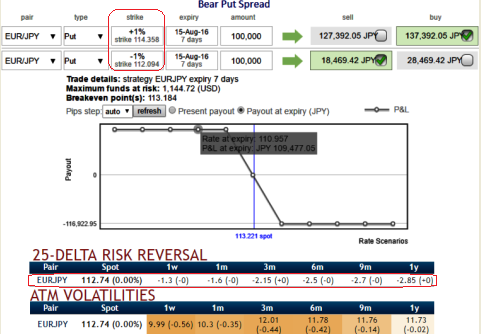

As the delta risk reversals have again shown in bearish interests as the progressive increase in negative numbers signify the traction for hedging sentiments for further downside risks in both short and long term.

Amid the apprehensions on perimeters of the policy arsenal at the BoJ and rising euro-centric risks, we recommend initiating short EURJPY positions for long-term hedging but by capitalizing on every short-term upswing, preferably via options during upcoming ECB meetings.

Until there is real domestically-generated inflation, it is hard to call EUR sustainably higher. Eventually, we think EUR recovers but it will be in a snail’s pace.

Well, in order to benefit from a favourable market move up to the higher strike:

As shown in the diagram for pay-off function of a debit put spread of EURJPY, below factors are indicative as to how it works at expiry, one of the following scenarios may occur:

1) Underlying trades below the lower strike then you sell the notional amount at the lower strike.

2) Underlying trades at or above the lower strike and below the higher strike, no transaction takes place on the settlement date. You could sell the notional amount at the prevailing spot rate (outside this structure).

3) Underlying trades at or above the higher strike, then you are obliged to sell the notional amount (multiplied by the leverage factor, if any) at the higher strike. Your profit potential is limited at the higher strike.