Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

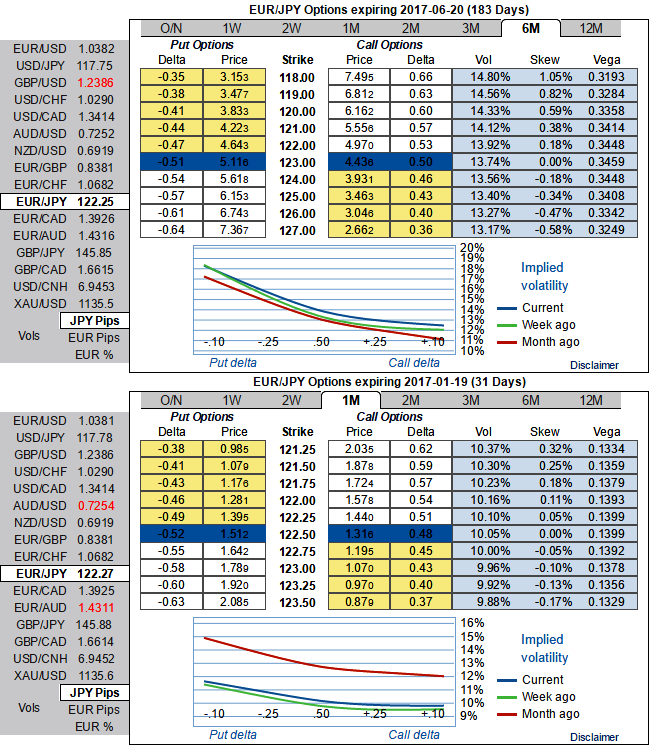

The BoJ maintains status quo in its monetary policy, it seems that the central bank is focused soothing 10Y Treasury bond yield, the benchmark for long-term borrowing costs, at around zero pct and keep the overnight interest rate around -0.1%. and asset purchases program at ¥80 trillion.

Although you could spot out positive changes in 1m risk reversals and ongoing spikes in the underlying spot, the positively skewed 1m IVs would still keep us alerted on downside risks and same has been the case with 6m skews.

As a result of the short-term bullish swings and major bearish pressures caused firstly by the European central bank with its soft taper as well Bank of Japan’s status quo, we devise below option strategy in order to monitor both puzzling swings.

The diagonal bear put spread strategy is recommended that involves buying long-term puts and simultaneously writing an equal number of near-month puts of a lower strike.

The strategy is constructed at net debit but with a reduced cost by writing (1%) 1m OTM put option, simultaneously, buying (1%) 6m ITM +0.67 delta put options. The Delta represents the option’s equivalent position in the underlying market. A higher (absolute) Delta value is desirable for an option buyer as the holder of an option looks for their option to be more valuable.

We’ve chosen ITM longs because an option moves further in-the-money in 3-months' span, the Delta’s absolute value rises and it becomes more valuable on every corresponding pips (or points) movement in the underlying spot FX.

This strategy is typically employed when the options trader is bearish on EURJPY spot FX over the longer term but is neutral to mildly bullish in the near term that is stated above.