Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields

The US continues to lag the growth upgrade cycle, prompting yet another 2% downgrade to the USD TWI forecast. Following some up and down, yesterday was a quiet day for the US currency. The ICE’s USD index traded in a range of 91.75 / 92.10. Even though the data due for publication today, the producer prices (PPI), affect inflation development and thus provide information for the market outlook on the Fed and the USD development we nonetheless do not expect the market to react to the data.

The USD rebound appears to be stalling and if the rally is to gain any further traction, it will need help from the US data (CPI and retail sales data due Thursday and Friday respectively) to give US yields an additional boost and light a fire under Fed Dec rate hike expectations.

On the flip side, SNB is scheduled for its Libor rate announcement on Thursday and you can foresee bearish scenarios of CHF given the fact that SNB resumes FX intervention at higher spot rates than previously and can be bullish if SNB desists from intervention over a multi-month period. Potential trigger events are SNB intervention (weekly sight depos, monthly stats, P&L on Swiss reserves).

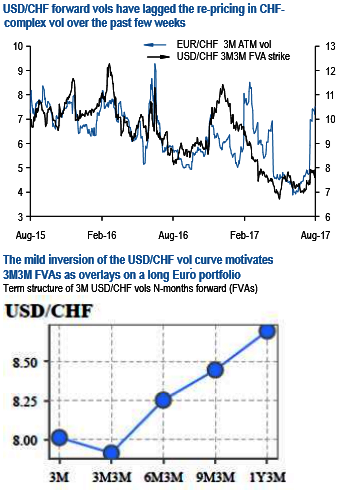

USDCHF 3M3M FVAs have lagged the upturn and are value buys along a mildly inverted curve. Holding USDCHF vol appeals because it can benefit from the full gamut of risk triggers that can afflict all USD-vols, is a useful hedge overlay on a bullish Euro macro portfolio, and retains exposure to idiosyncratic CHF weakness of the kind seen recently, all without the threat of overt SNB management that can frustrate outsized sell-offs in EURCHF.

The FVA format is motivated in part by the fact that USDCHF forward vols have severely lagged the surge in CHF-complex gamma (refer above chart), and partly by the mild inversion of the vol curve that ensures optically appealing flat slide/roll over time (refer above chart).

Admittedly some of the term structure shape is due to the forward starting 3M window covering the quiet holiday weeks of late December (3M3M = mid-November’17 to mid-February'18) that depresses 6M vol, but despite that, it may not be the worst idea to take delivery of and own USDCHF straddles through the first half of December that can reprise the above-average volatility of previous years around ECB and Fed meetings when tapering and rate hike decisions are expected to be announced.