Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Today’s Turkish central bank’s monetary policy hasn’t been driving force for lira. CBT maintained status quo policy by keeping its benchmark one-week repo at 8.25 percent as widely expected, this was the unanimous expectation in the market that CBT would leave its benchmark rate on hold at 8.25%. In a fundamental sense, there is no rationale for cutting rates at this time: the economy is pulling out of its corona dive; activity remains well below normal level, but is, at least, improving month-on-month in most sectors. Inflation, on the other hand, shows no sign of moderating – the noticeable acceleration in core inflation during June led the central bank to suspend its hitherto uninterrupted rate cutting cycle; at the time.

After the country's headline inflation rate hit the highest level for 10 months in June boosted by a surge in food inflation due to seasonal and pandemic-related effects, while commodity prices continued to restrain consumer prices. Policymakers said that demand-driven disinflationary effects will become more prevalent in the second half of the year as the normalization process continues, while the economic recovery will continue helped by recent monetary and fiscal measures.

CBT even acknowledged that cumulative lira depreciation was the reason behind this inflation acceleration, an assessment we absolutely concur with. This fundamental factor has not reversed since – the only thing which has changed significantly is that the economy needs less emergency support, not more – hence, it makes sense to expect that rates will not be cut right away.

We, however, expect further rate cuts down the road – in fact, the central bank governor too has conceded that rates will be cut again during H2 when inflation begins to moderate. We do not forecast inflation to moderate to anywhere near CBT’s projections; but besides fundamental improvement, there could be other forces which kickstart another easing cycle – the main one being pressure from President Tayyip Erdogan. If economic activity were to remain subpar in coming months, instead of rebounding powerfully back to year ago levels or better, Erdogan will very likely pressure the central bank once again. This is the scenario we find more likely and, at the same time, concerning from the viewpoint of the lira exchange rate.

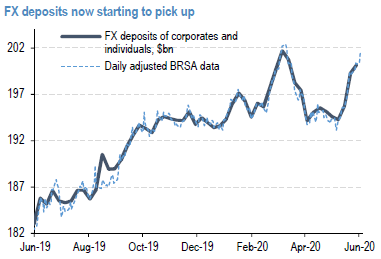

In TRY, we stay UW and added a 6-month USDTRY forward as we reckon BoP pressures are likely to prove key for lira’s outlook. Short-term external debt repayment needs remain high, although admittedly the rollover schedule is lighter over July-September. Portfolio outflows have reached $10.3bn YTD (see here) and while a recovery in global risk appetite is likely to slow non-resident selling, we believe portfolio flows are likely to remain subdued. Dollarization now appears to be picking up (refer above chart).

Finally, our economist forecasts a 0.8% GDP current account deficit in 2020. Given the better than expected growth performance and the high credit growth risks are for a larger deficit.

Hence, contemplating above factors, we advocate activating longs in Dec’2020 USDTRY forwards for target upto 8.25 with strict stop loss at 6.60 levels. Courtesy: Commerzbank