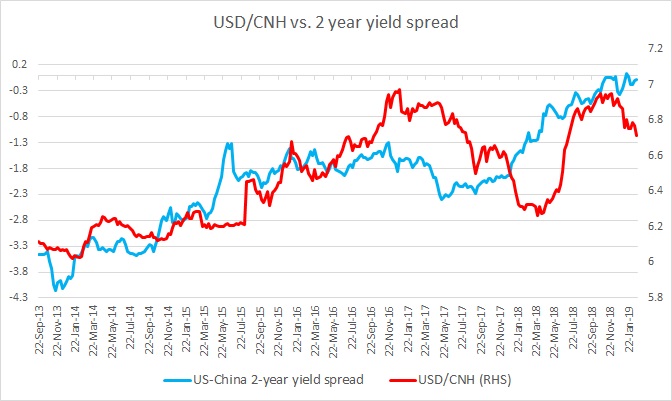

Brief background:

- This chart shows the relation between the U.S. - China 2-year yield spread and the Dollar/Chinese yuan exchange rate since 2013. It is visible even with naked eyes that the two has enjoyed a very close relationship. It can also be seen that the infamous August 2015 devaluation of the Chinese yuan by the People’s Bank of China (PBoC) that led to a global financial turmoil could very well be the result of rising U.S./China 2-year spread.

- Since March 2015, the yield spread between the United States and China’s 2-year bond rose from -276.6 basis points to -131.3 basis points in favor of the dollar by June, while the exchange rate was kept flat around 6.2 per dollar. Finally, PBoC had to respond with a one-time devaluation of the yuan to 6.46 for per dollar. This shows, how significant the spread is for the pair.

Past reviews:

- In our review in mid- September 2017, we pointed to the spread to explain the recent strengthening of the yuan against the USD. We noted that since the U.S. election, the yield spread has widened from -129 basis points to -216 basis points in favor of the yuan. Naturally, the exchange rate has responded by declining from 6.95 per dollar to 6.54 per dollar.

- In our October review, we noted that the yield spread has narrowed from 216 basis points to 206 basis points in favor of the dollar and the yuan has weakened around 90 pips against the dollar. The exchange rate is currently at 6.64 per dollar. We can see that the exchange rate has corrected more, creating a small divergence.

- In our November review, we noted that the yield has only moved by 1.1 bps in favor of the yuan and the yuan has strengthened from 6.65 per dollar to 6.623 per dollar.

- In our January 2018 review, we noted that a large divergence has set in. Since the review in early November, the spread (US-China) has narrowed from 205 bps to 152 bps, however, the yuan has strengthened from 6.623 per dollar to 6.329 per dollar.

- By April, the spread has narrowed from 152 bps to 75 bps as of today in favor of the dollar, whereas the Chinese yuan has strengthened from 6.33 per USD to 6.3 per USD.

- In August, as anticipated, the Chinese yuan has finally started responding to the widening yield spread between the U.S. and China by declining at a rapid pace. The chart clearly showed that the divergence between the yield spread and the exchange rate is now largely reduced.

- In September, we saw that the exchange rate is struggling to find direction as the spread is not narrowing in favor of the USD anymore.

- In the October review, we noted that the yield spread and the exchange rate is moving hand in hand. As the yield spread rose in favor of the USD, yuan weakened against the dollar. The spread narrowed by 25 bps to -25 bps, and yuan weaned from 6.84 to 6.94 per USD.

- In November, the spread narrowed further sharply from -25 bps in the last review to -3 bps but the yuan’s decline has not been that sharp. The yuan is currently trading at 6.953 against the USD.

- In our December review, we noted that from November to December, the spread has reversed course and declined sharply favoring a stronger yuan. The spread declined from -3 bps to -30 bps but the yuan was broadly unchanged at 6.91 per USD, which suggested that a decline in USD/CNH could be around the corner.

- In the January review, we noted that a strong divergence is taking place. While USD/CNH has corrected to 6.8 per USD, the yield spread narrowed from -30 bps to -7 bps in favor of the USD. If the spread continues to widen in favor of the USD, the yuan may face rapid decline.

Current analysis:

- Since our last review, after a brief correction (spread widened to -18 bps in favor of the yuan), it has narrowed again to -8 bps. However, USD continue to weaken against the yuan and currently trading at 6.7 per USD. Such divergence would be unsustainable in the medium term. The risk of a sharp recovery in USD against yuan remains likely.