Trump Pushes China Market Access During High-Stakes Xi Summit

Trump Pushes China Market Access During High-Stakes Xi Summit  Trump, Xi Begin High-Stakes China Summit Focused on Trade, Taiwan and Global Tensions

Trump, Xi Begin High-Stakes China Summit Focused on Trade, Taiwan and Global Tensions  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions

Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions  DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  US Stock Futures Slip as Iran Tensions and Hot Inflation Data Pressure Wall Street

US Stock Futures Slip as Iran Tensions and Hot Inflation Data Pressure Wall Street  OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027  Asian Currencies Slide as Indian Rupee Hits Record Low Amid Iran Tensions

Asian Currencies Slide as Indian Rupee Hits Record Low Amid Iran Tensions  Japan Considers Extra Budget Aid Amid Rising Fuel and Utility Costs

Japan Considers Extra Budget Aid Amid Rising Fuel and Utility Costs  Gold Prices Hold Steady as Investors Monitor U.S.-Iran Tensions and Trump-Xi Summit

Gold Prices Hold Steady as Investors Monitor U.S.-Iran Tensions and Trump-Xi Summit

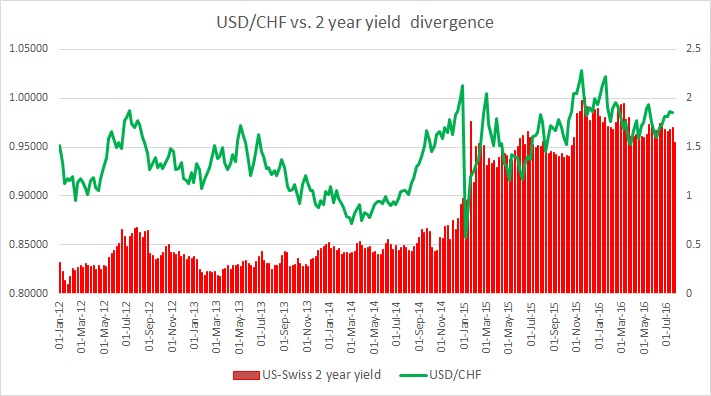

In recent days, Swiss franc’s correlation with the 2-year yield spread (US-Swiss 2 year) has dropped to 25 percent but time on time again it shows relatively high positive correlation, as high as 80 percent at times. Just before and after the Brexit referendum in the UK, the 20-day rolling correlation was averaging above 60. Hence, it is vital to keep a watch on the Swiss yields.

Just after the Swiss floor shock in January 2015 when the Swiss National Bank (SNB) removed a floor in EUR/CHF at 1.20 this relation went to negative and stayed there until October with occasional bounces to positive territory. It hasn’t gone to the negative since and was closely related to the yield (above 80 percent) in January this year.

Unlike the euro or the pound, the Swiss franc is considered a safe haven, hence the yield relation sometimes gets overlooked.

However, Swiss yields are a must watch as they are the lowest for any government bonds in the world and any shift in that will mark a major turnaround in trend. The above chart explains how the relation between the spread and exchange rate has unfolded since 2012.