Trump, Xi Begin High-Stakes China Summit Focused on Trade, Taiwan and Global Tensions

Trump, Xi Begin High-Stakes China Summit Focused on Trade, Taiwan and Global Tensions  Dollar Surges as Inflation Data Fuels Fed Rate Hike Expectations

Dollar Surges as Inflation Data Fuels Fed Rate Hike Expectations  Havana Protests Erupt as Cuba Faces Severe Blackouts and Fuel Crisis

Havana Protests Erupt as Cuba Faces Severe Blackouts and Fuel Crisis  Trump Says Iran Ceasefire ‘On Life Support’ as Oil Prices Surge Above $104

Trump Says Iran Ceasefire ‘On Life Support’ as Oil Prices Surge Above $104  Oil Prices Hold Above $100 as Trump-Xi Meeting and Iran Conflict Keep Markets on Edge

Oil Prices Hold Above $100 as Trump-Xi Meeting and Iran Conflict Keep Markets on Edge  US Stock Futures Slip as Iran Tensions and Hot Inflation Data Pressure Wall Street

US Stock Futures Slip as Iran Tensions and Hot Inflation Data Pressure Wall Street  Wall Street Futures Rise Ahead of Trump-Xi Summit as Tech Stocks Lead Market Rally

Wall Street Futures Rise Ahead of Trump-Xi Summit as Tech Stocks Lead Market Rally  Trump Faces Uphill Battle Seeking China’s Help on Iran Conflict

Trump Faces Uphill Battle Seeking China’s Help on Iran Conflict  US-China Trade Talks Begin in South Korea Ahead of Trump-Xi Beijing Summit

US-China Trade Talks Begin in South Korea Ahead of Trump-Xi Beijing Summit  Oil Prices Slip as Strait of Hormuz Disruptions and U.S. Inventory Data Keep Markets on Edge

Oil Prices Slip as Strait of Hormuz Disruptions and U.S. Inventory Data Keep Markets on Edge

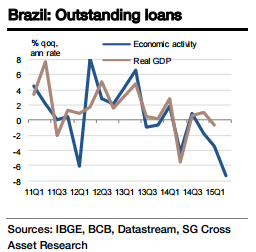

Brazil's economic activity index suggests that the supply-side economy contracted -7.3% qoq (annualised ) or -3.1% yoy in Q2.

"This prompts to project Q2 GDP growth of -1.7% qoq (-7.0% annualised or -2.7% yoy for the non-seasonally adjusted series), which is not significantly different from the earlier forecast. Yet, the economy seems to be heading for a worse contraction than it was expected until just a couple of months back. Both private and public consumption look in worse shape with the anticipated and significant fiscal drag from H2 and inflation set to continue to rise", Societe Generale.

Moreover, data through Q2 show no evidence of investment bottoming despite some gains on the export front (in volume terms) - primarily due to the depreciating currency. The lagged effect of higher interest rates will continue to exert downward pressure on investment, particularly in the current environment where confidence is extremely low.

"Assuming the fiscal situation remains stressed and the unemployment rate continues to rise, the economy will contract -2.1% in 2015 followed by -0.1% in 2016. The only upside, at this stage, could be a potential revival through trade channels. However, we are hesitant to take big bets on this as of yet", states SocGen.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Brazil GDP likely to contract heavily in Q2

Friday, August 28, 2015 6:08 AM UTC

Editor's Picks

- Market Data

Most Popular