Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Gold Prices Hold Steady as Investors Monitor U.S.-Iran Tensions and Trump-Xi Summit

Gold Prices Hold Steady as Investors Monitor U.S.-Iran Tensions and Trump-Xi Summit  Oil Prices Hold Above $100 as Trump-Xi Meeting and Iran Conflict Keep Markets on Edge

Oil Prices Hold Above $100 as Trump-Xi Meeting and Iran Conflict Keep Markets on Edge  BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance

BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance  US, Japan Reaffirm Strong Currency Coordination Amid Yen Volatility

US, Japan Reaffirm Strong Currency Coordination Amid Yen Volatility  Trump and Xi Temple of Heaven Visit Highlights Trade and Diplomacy Goals

Trump and Xi Temple of Heaven Visit Highlights Trade and Diplomacy Goals

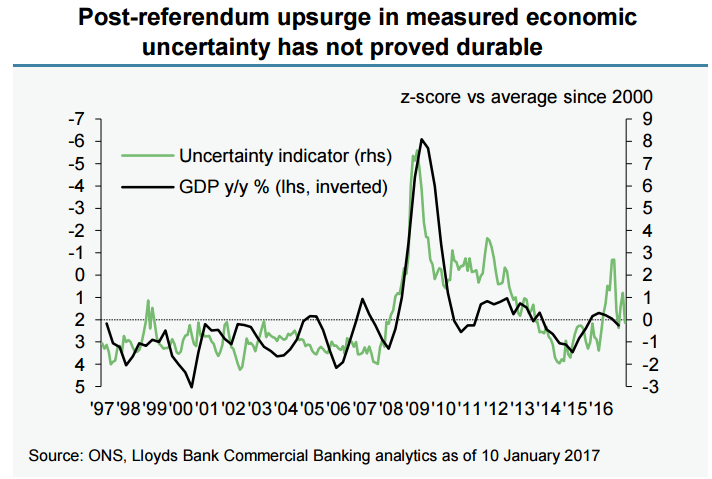

Incoming economic data in UK do not support the view of an uncertainty driven slowdown in the aftermath of the EU referendum. UK economy expanded at 0.6 percent q/q in Q3 2016, the first full post-referendum quarter. The economy’s dominant services sector saw a brisk 1.0 percent q/q growth in Q3.

Composite PMI in December spanning across the manufacturing, construction and services sectors stood at its strongest since July 2015. Survey data for Q4 have also been solid and analysts expect overall GDP growth in Q4 could post a 0.5 percent q/q rise. Together with the recent history of GDP data, that would leave growth in the six months since the referendum, in fact, quicker than in the first half of 2016. And the apparent resilience towards the end of 2016 suggests that some of this momentum is likely to carry over into H1 2017.

Inflation in the UK is likely to rise through 2 percent target by spring 2017 as currency weakness drives import price rises. The coming few months are likely to see a sharp rise in the headline inflation rate on the back of significant impact from energy price base effects and as the exchange rate pass-through becomes dominant.

"We expect CPI inflation to tick up further to 1.3% by December and burst through the 2% target by spring 2017. Easing underlying cost pressures from the second half of 2017 should provide some offset as growth in the economy slows modestly and reduced labour market tightness limits inflation’s overshoot relative to target." said Lloyds bank in a report.

As exit negotiations with the European Union begin, how measures of uncertainty evolve over the coming months and how strong the mapping proves with official activity data are among the key questions for the near-term outlook. The deceleration of economic activity over the course of 2017 and 2018 is likely to principally result from the weakness of sterling.

UK Monetary Policy Committee (MPC) is likely to look through inflation rise, but could react if activity slowdown proves more modest than expected. "Our base scenario sees Bank Rate on hold for the foreseeable future, but with a skew towards tighter policy," adds Lloyd's Bank in a report.

GBP/USD tests 1.21, weakest since Oct 7 'flash crash'. Cable continued slump as Hard-Brexit concerns continued to weigh on the investors’ sentiment. EUR/GBP spiked beyond 0.8750 to hit fresh multi-week highs at 0.8763.

FxWirePro Currency Strength Index showed Hourly GBP Spot Index at -91.9716 (Highly Bearish) at 1130 GMT. For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex.