Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations

Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations  Japan Signals Readiness to Act on Yen as Intervention Speculation Grows

Japan Signals Readiness to Act on Yen as Intervention Speculation Grows  Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears

Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears  Wall Street Ends Mixed as Weak Jobs Data Lowers Fed Rate Hike Bets, Chip Stocks Tumble

Wall Street Ends Mixed as Weak Jobs Data Lowers Fed Rate Hike Bets, Chip Stocks Tumble  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms  China Services PMI Beats Forecasts as Strong Demand Supports June Growth

China Services PMI Beats Forecasts as Strong Demand Supports June Growth  Asian Stocks Slide as Chip Shares Tumble Ahead of Key U.S. Jobs Report

Asian Stocks Slide as Chip Shares Tumble Ahead of Key U.S. Jobs Report  US Dollar Rises as Fed Rate Outlook Stays Hawkish, Euro Slips and Yen Near 40-Year Low

US Dollar Rises as Fed Rate Outlook Stays Hawkish, Euro Slips and Yen Near 40-Year Low  U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk

U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk  Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens

Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

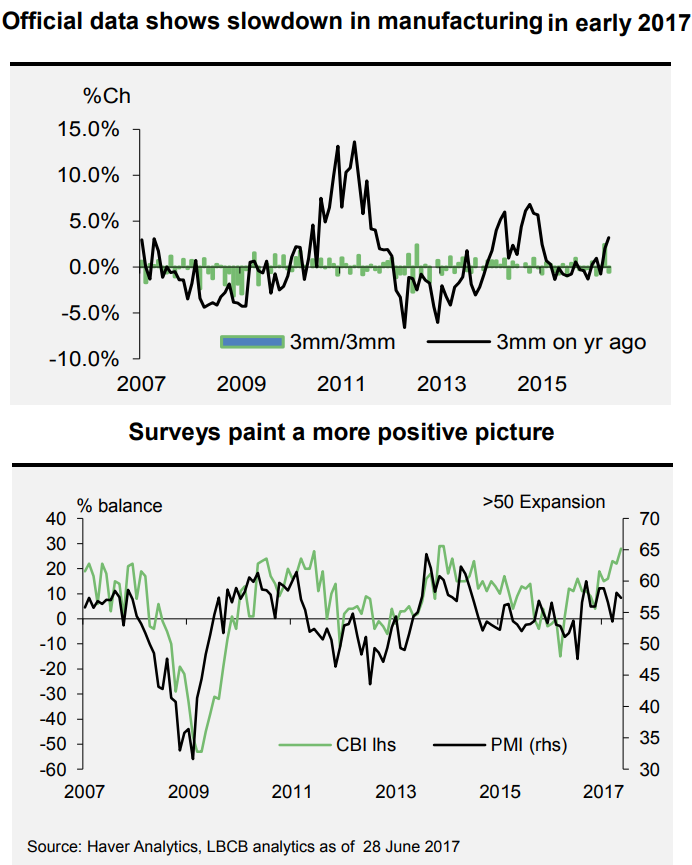

UK second quarter started off on a bad note as the manufacturing and construction sectors performed poorly in April. Office for National Statistics data showed that manufacturing rose by just 0.2 percent in the month, while construction output dropped by 1.6 percent. The drop came in despite purchasing managers’ index surveys suggesting an improvement in momentum in April. Data suggests that GDP growth in Q2 may not see a big improvement as previously thought.

That said, the extent of slowdown is probably exaggerated as it follows what looks to have been erratically strong rises in November and December of year 2016. Manufacturing activity has picked up across a number of other economies in the eurozone in the recent months. The US also started the year on a firm footing. This suggests that there has been a rebound in demand for manufactured goods

Business surveys also point to a rise in export orders which indicates that international demand for UK manufactured goods is rising. UK trade data showed that exports stayed flat at £49.8bn in April while imports dipped from £53.7bn to £51.9bn, narrowing the deficit to £2.1bn. Volatility in monthly trade data cannot be ruled out as large orders of goods such as aircraft can sway the national figures. A combination of stronger world trade growth and the competiveness boost that should follow from sterling’s depreciation of last year are positive signals for manufacturing exports.

Meanwhile, manufacturing continues to face a number of headwinds including difficulties in recruiting staff, sluggish productivity growth and ongoing concerns about the impact of Brexit. Employers face a triple whammy of uncertainty over the last few months – a snap election, the triggering of article 50, and weak economic data for the first half of 2017. Surveys showed stark contrasts between sectors. Manufacturers were most optimistic about hiring but the outlook for the public sector was far gloomier, with a majority of employers looking to cut jobs.

"Recent manufacturing performance has been patchy due to variable impacts from sterling depreciation, a slowing domestic market and an uneven international upturn. Business surveys, however, paint a rosier picture including robust orders growth. This suggests that any slowdown will be temporary," said Lloyds Bank in a report.

GBP/USD was trading range bound at around 1.2819 at 1145 GMT. Technical indicators are bullish and we see scope for further gains. The pair closed above 20-day MA and now finds stiff resistance at cloud top. Break above will confirm further bullishness. FxWirePro's Hourly GBP Spot Index was at 31.8402 (Neutral), while Hourly USD Spot Index was at -61.7679 (Slightly bearish). For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit http://www.fxwirepro.com/invest