China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

While Draghi usually displays an impressive mastery of the press conference, he has had "communication mishaps" in the past. If he comes out too hawkish next week, ie, too dismissive of the risks, the euro exchange rate could undergo a knee-jerk leap, which would make waiting until 3 December quite taxing for the Euro area.

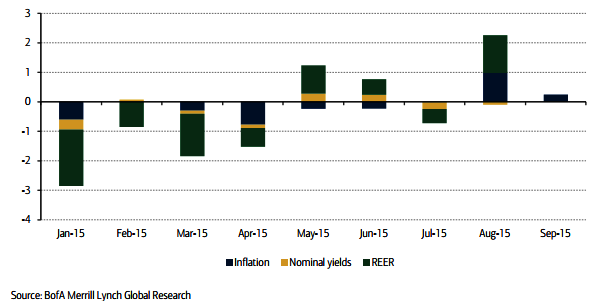

Without a quick response from the ECB, we believe the new configuration for world demand combined with tightened financial conditionscould cost the Euro area's GDP growth 0.2/0.3ppt, still leaving a decent pace (above potential) but with no acceleration relative to this year.

"The acceleration of our forecasts from 1.6% GDP growth in 2015 to 1.9% in 2016 was mainly driven by a pick-up in capex from 2.0% to 2.7% (Table 2). This was expected to be fuelled by re-emergence of the lending cycle with abundant liquidity, expectations of decent growth for a couple of years, and real rates at their lowest levels for a while", says Bank of America.

This would certainly at least be questioned if the ECB response was not fast and/or strong enough. And in contrast to May, the recent move has a lot to do with the evolution of real rates, which in turn have been driven by falling inflation expectations, together with the evolution of the currency.

This generalized tightening of monetary conditions was the main driver of our QE2 call for this year. If looked in particular at the long end of real rates, the important ones for the evolution of investment, since the lows in Q2 10Y real rates are up 30bp.

"If the ECB disappoints and real rates do not move much from where they are in the short run, that would cost the 20-30bp in terms of GDP for 2016 suggested above, since it would impact the evolution of investment in the next few quarters", added Bank of America.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Tighter conditions until December could harm Euro area growth

Wednesday, October 21, 2015 3:32 AM UTC

Editor's Picks

- Market Data

Most Popular