South Africa Eyes ECB Repo Lines as Inflation Eases and Rate Cuts Loom

South Africa Eyes ECB Repo Lines as Inflation Eases and Rate Cuts Loom  Federal Reserve Faces Subpoena Delay Amid Investigation Into Chair Jerome Powell

Federal Reserve Faces Subpoena Delay Amid Investigation Into Chair Jerome Powell  RBA Raises Interest Rates by 25 Basis Points as Inflation Pressures Persist

RBA Raises Interest Rates by 25 Basis Points as Inflation Pressures Persist  ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence

ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence  Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness

Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness  MAS Holds Monetary Policy Steady as Strong Growth Raises Inflation Risks

MAS Holds Monetary Policy Steady as Strong Growth Raises Inflation Risks  Bank of Canada Holds Interest Rate at 2.25% Amid Trade and Global Uncertainty

Bank of Canada Holds Interest Rate at 2.25% Amid Trade and Global Uncertainty  Fed Governor Lisa Cook Warns Inflation Risks Remain as Rates Stay Steady

Fed Governor Lisa Cook Warns Inflation Risks Remain as Rates Stay Steady

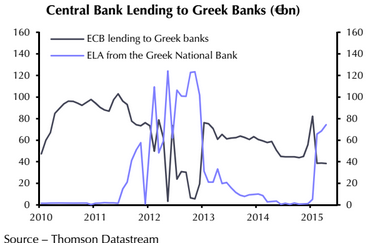

The ECB's exposure to Greece is not huge and ultimately lies with the euro-zone governments that would have to recapitalise it. But a Greek default to the ECB would be a serious blow to the Bank's credibility that could limit its ability to control inflation or support stressed bond markets in future.

The ECB is exposed to a Greek default through two direct channels. Its holdings of Greek government bonds purchased during the Securities Markets Programme (SMP) have a book value of €18bn, or 0.2% of euro-zone GDP. Chart shows that €6.7bn worth matures this summer. And its lending to Greek banks through refinancing operations was €38.5bn (0.4% of GDP) in April. So in the event of a sovereign default and associated collapse of the banking sector, the ECB could suffer losses of up to €56.5bn, wiping out its subscribed capital of €10.8bn, but not its total capital and reserves of €96bn, notes Capital Economics.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

How vulnerable is the ECB to a Greek default?

Thursday, May 28, 2015 9:01 AM UTC

Editor's Picks

- Market Data

Most Popular