China Inflation Jumps as Iran Conflict Drives Energy Costs Higher

China Inflation Jumps as Iran Conflict Drives Energy Costs Higher  Asian Stocks Rise Despite Middle East Tensions as Chipmakers Boost Markets

Asian Stocks Rise Despite Middle East Tensions as Chipmakers Boost Markets  Japan’s Yen Intervention and BOJ Rate Hike Bets Support Currency Recovery

Japan’s Yen Intervention and BOJ Rate Hike Bets Support Currency Recovery  Wall Street Hits Record High as AI Chip Stocks and Strong U.S. Jobs Data Boost Markets

Wall Street Hits Record High as AI Chip Stocks and Strong U.S. Jobs Data Boost Markets  Oil Prices Rise Amid Strait of Hormuz Tensions and U.S.-Iran Ceasefire Uncertainty

Oil Prices Rise Amid Strait of Hormuz Tensions and U.S.-Iran Ceasefire Uncertainty  South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Trump Rejects Iran Proposal as Strait of Hormuz Crisis Pushes Oil Prices Higher

Trump Rejects Iran Proposal as Strait of Hormuz Crisis Pushes Oil Prices Higher  AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

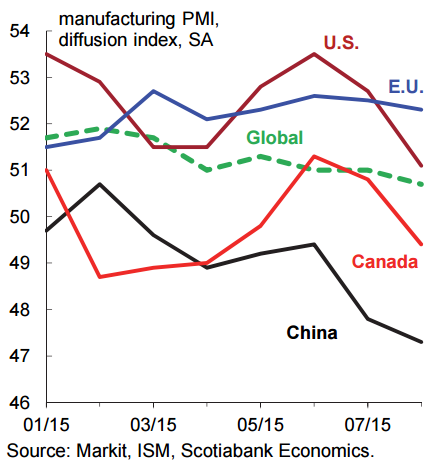

The Chinese economy is in slowdown mode, global markets and the economies linked to China's growth face further challenges. Downward bias in commodity prices, and the renewed increase in financial market turbulence are risking further weakness. Financial market volatility around the world has increased dramatically in recent weeks. Sell-off in global stock markets, followed by only a partial rebound, continues to grind lower and highlights a downgraded assessment of economic conditions and corporate earnings.

In this environment, business investment is at risk of a further slowdown in response to the increased economic uncertainty, the absence of a discernible pick-up in global demand and trade. Accordingly, prospects for global growth are likely to remain on the softer side for the time being. The biggest downside risks are in the resource-sensitive regions.

Many emerging markets and developing nations are being negatively affected by the combination of the slowdown in China, the decline in commodity prices, persistent U.S. dollar strength, the intensifying weakness in currency and financial markets. Investor confidence around the world is being challenged. There are not enough growth engines around the world. Only the U.S., the U.K. and India can be considered relative outperformers, countries which appear to be the most resilient and have the potential to generate stronger, and importantly, more sustainable activity.

Moderate growth and weak prices for many key commodities besides oil are reinforcing the likelihood of a more prolonged period of very low overall inflation. Increasingly, more and more policymakers around the world are favouring easier credit conditions and weaker domestic currencies to provide some relief. The Fed is poised to raise short-term interest rates, but the timing and extent of prospective rate hikes will depend upon the strength of the U.S. expansion and 'core' inflation, and the potential for any spillover from the volatile financial market and economic conditions around the world.

"The price of WTI crude oil recently reversed its spring-time run-up, and is currently trading nearer the lower end of a US$40-60/barrel range this year. Geopolitical events and recurring volatility aside, underlying fundamentals suggest that crude oil prices will likely remain on the weaker side for longer", says Scoitabank in a research note to its clients.

The current softness in the global economy is expected to give way the renewed economic traction as the drag from structural adjustments and financial market instability abates. Considerable pent-up demand in the U.S. should underpin steady consumer spending and housing-related gains.

Increasing monetary and fiscal stimulus should help stabilize conditions in China. Persistently low borrowing costs and low oil prices remain supportive of improved economic performances internationally. And in contrast to the Great Recession, many banks around the world are much better capitalized and capable of financing increased activity.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Global growth slowdown persists

Wednesday, September 2, 2015 10:37 AM UTC

Editor's Picks

- Market Data

Most Popular