Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell

Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Following the initial flash crash earlier last Friday, the Turkish lira appeared to be stabilized for a while before it continues to depreciate slightly again. The lira is not alone in this: currencies such as the forint have weakened as well in this general risk-off environment.

However, we should note that in the case of the lira at least, initial depreciation often 'catches fire' later because the market wants to 'test CBT's resolve' – this has become a standard market theme since 2013 as CBT has typically been reluctant to raise rates. This tends to kick-start a spiral between TRY depreciation and inflation, which then results in significant FX overshooting.

In this manner, an externally-driven currency move ends up acquiring a 'life of its own'. Depending on how far things go, CBT may or may not be forced to respond with emergency rate hikes.

While the defensive tactic of using high carry to subsidize the cost-of-carry of long vol is more appropriate to apply to currencies like TRY at the other end of the spectrum, where the macro standpoint seems to be bearish.

Funding the current account deficit makes lira vulnerable in periods of low global risk appetite. Strong portfolio inflows of around $20bn helped finance the current account deficit in 2017. The potential for a global environment of lower risk appetite, with the recent equity market volatility and rising DM rates, may dampen international investor appetite.

The EMEA analysts note that real yields in Turkey are still too low to sustainably bring down inflation, the current account deficit continues to widen, and the likelihood of comfortably funding the BoP through a repeat of 2017’s heavy portfolio inflows are slim.

More than outright long vega, bearish TRY views are well expressed through partially delta-hedged risk-reversals, in our stance.

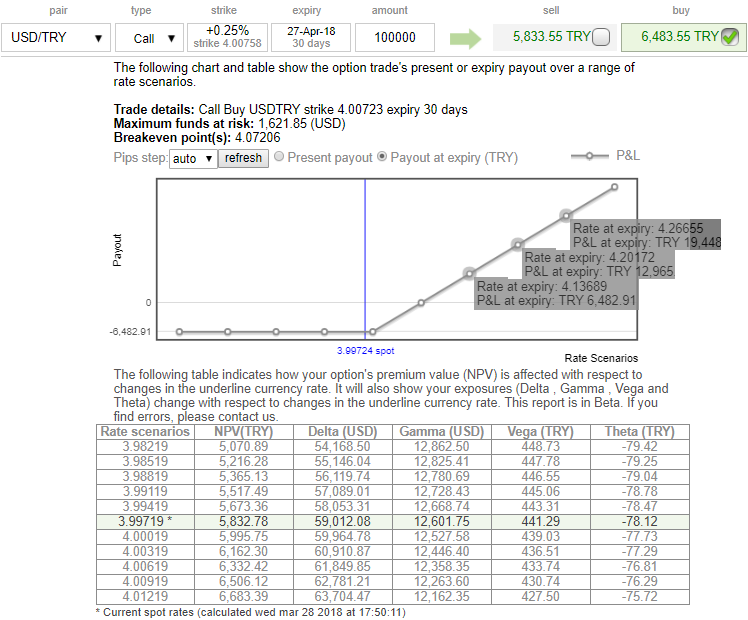

Overall, the lira hasn’t been more volatile but steadily bearish recently, and therefore the tendency for inflation will be to peak and moderate – but only slightly, say to around 9% in the coming months. This extent of moderation will not neutralize Turkey’s long-term inflation, though – at best, it can bring near-term relief. As stated in our previous post the underlying spot FX has hit 4.00 mark In the medium-term term, we, therefore, expect USDTRY to head up towards the 4.0350 mark.

Hence, we add to our bearish TRY position as a hedge to rising core yields with a deteriorating current account balance adding challenges to the lira outlook.

Trading tips:

We had advocated buying USDTRY +0.59 delta call (4.00) and EURTRY call (4.83) (equal weighted USD notional), we wish to roll on the same positions using near-month tenors on hedging grounds ahead of lingering potential upside risks (refer payoff structure for exponential effect in yields as the underlying spot FX keeps rising).

FxWirePro launches Absolute Return Managed Program. For more details, visit: