Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

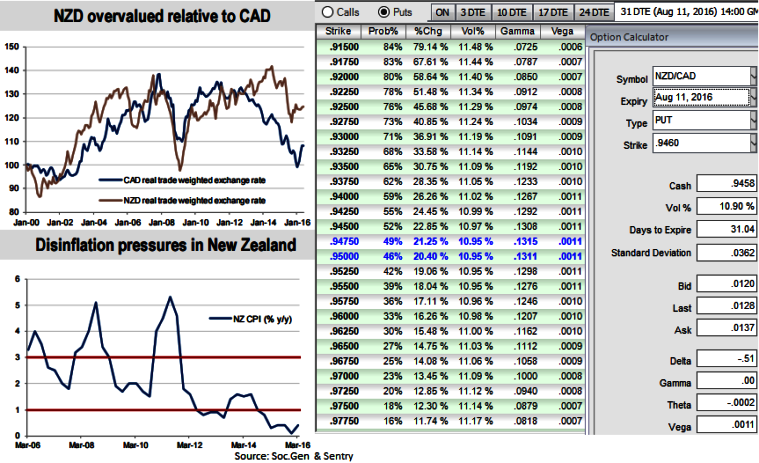

NZD remains overvalued, while milk powder prices have stayed depressed and inflation in New Zealand has surprised to the downside.

New Zealand is suffering from disinflationary pressures, with reported CPI inflation well below the RBNZ’s 1-3% target range (see above graph). It is also more exposed to China growth risks than Canada.

On the data front, NZ’s data calendar next week again holds little importance for markets.

We have REINZ housing update for June, electronic spending (Mon), food prices (Wed), manufacturing PMI, and ANZ consumer confidence (all Thu).

More closely read will be the speech from RBNZ Asst. Gov. McDermott on Wed, on how they decide the OCR, although the bulletin has partly stolen the thunder.

On the flip side, an expected, a plateauing of the oil price trend going forward also eliminates what has been one of the key factors behind CAD strength in the first half of the year. But CAD offers good long-term value, and investors should look to fade any sustained weakness in the coming months.

The Canadian dollar offers better value, and should continue to benefit from more stable crude oil prices and the US economic recovery.

1M ATM IVs are stable just shy below 11% and the sensitivity tool suggests OTM put strikes are on upper hand.

Thus, maintaining shorts in NZD/CAD is a relative value trade with low correlation to global market trends.