China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

Bullish Scenarios see USDCAD above 1.45 levels if:

1) A second COVID-19 wave catalyses another global sudden-stop and aggravates Canada’s external deficits or

2) The renewed oil price war or demand shock drives additional industry-wide crude production shut-ins.

3) US-China tariff war restarts.

Bearish Scenarios see USDCAD below 1.30 levels if:

1) The COVID recovery is complete (V-shape to 2019 total output).

2) The quicker than expected resolution of the COVID-19 crisis via comprehensive health solution (treatment & vaccine) allowing a quicker economic recovery.

Disproportionately large repatriation by residents helped support Canada’s BoP during the March panic, but external financing vulnerabilities remain a potential drag for CAD, with the ability to attract ongoing inflows impaired post-COVID crisis. Incoming data in the past month shed better light on flows supporting CAD’s relative resilience during the peak of the COVID panic (compared to some other high-beta and petro-FX peers). Recently released March international portfolio flows data show 1.4% of GDP worth of net portfolio inflows in March alone helping offset some of the excess USDCAD demand during the peak of the crisis.

Hence, we make mark-to-market to our USDCAD projections following the recent sizable USD weakness, but maintain an upward bias in the pair to reflect structural CAD headwinds over the 1y forecast horizon. Our near-term USDCAD forecasts are slightly lower than spot to reflect that USD weakness can persist if re-openings around the world continue to contribute a strong pro-growth environment and help buoy risk sentiment. But we believe that the structural drags in Canada will ultimately weigh on CAD over the medium-term, particularly as the local growth story remains bleak from oil and financing the joint C/A-FDI deficit will remain precarious given that Canada no longer enjoys 2019’s best-in-G10 yield advantage. We are also cognizant of longer-term economic forces (quasi-permanent economic scaring associated with dislocations in the labor markets, higher debt levels, the behavioural shifts from consumers and corporates) as well as medium-term risks like fiscal tightening amid an incomplete global recovery by year-end, in addition to tail risks of COVID second waves. As such, we project USDCAD to 1.38 by year-end, and 1.42 by 2Q’21.

Contemplating above factors, we maintain that directionality from here. It makes sense that CAD has focus on Canada's specific weaknesses grows larger.

Hence, add longs in USDCAD via options with diagonal tenors contemplating above fundamental factors and below OTC indications:

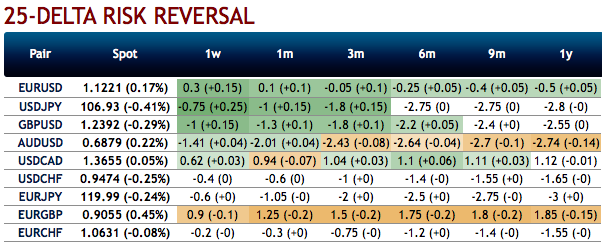

The fresh negative bids for 1m tenor to the existing bullish risk reversal setup indicate the broader hedging sentiments for the upside price risks amid minor hiccups in the shorter tenors (refer 1st chart).

While to substantiate this broader bullish hedging stance, we capitalize on the positively skewed IVs of 3m tenors that indicates the upside risks in in the longer tenors (see bids for OTM call strikes upto 1.41, refer 2nd chart).

Hence, at this juncture (spot reference: 1.3663 levels), we upheld our shorts in CAD on hedging grounds via 3m/1m (1.34/1.41) debit call spread. If the scenario outlined above unfolds, we will re-assess our stance but at the moment there are no changes to our CAD recommendations. Courtesy: Sentry, Saxo & JPM