US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Ahead of upcoming event risk, GBP prices have and are likely to continue to hold the range highs. Parliamentary developments ahead of next Tuesday’s “meaningful” vote will continue to dominate the domestic focus through today’s session, as we go into the third day of debates on the EU withdrawal agreement in the House of Commons.

On a broader perspective, a key risk to our bullish GBP view is that Brexit clarifications are dragged out - even beyond 30 March if Article 50 is extended, and the GBP appreciation consequently will be much more moderate and materialise later than our forecast (main scenario) implies.

Defeat of a Brexit motion in parliament causes the government to fall, paving wave for a general election and/or a second referendum and potentially no Brexit.

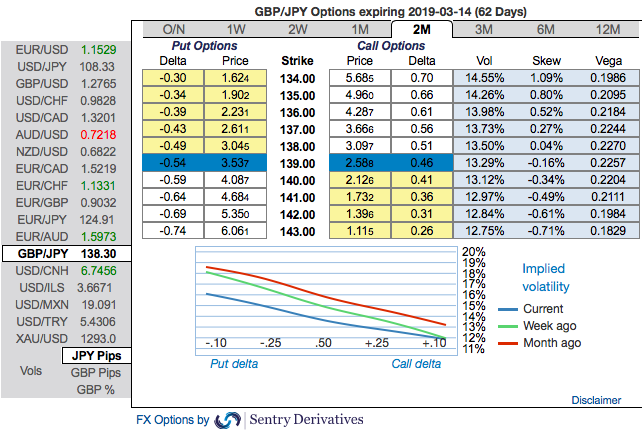

OTC outlook and Hedging Strategy: Please be noted that IVs of this pair that display the highest number among entire G10 FX universe (spiking above 13.52%). Hence, vega long put are most likely to perform decently capitalizing on rising mode of IVs.

While the positively skewed IVs of 2m tenors signify the hedgers’ interests to bid OTM put strikes upto 134 levels (refer above nutshells evidencing IV skews).

Accordingly, diagonalput ratio back spreads (PRBS)are advocated on the hedging grounds. Both the speculators and hedgers who are interested in bearish risks are advised to capitalize on current abrupt and momentary price rallies and bidding theta shorts in short run, on the flip side, 2m skews to optimally utilize delta longs.

The execution: Capitalizing on any minor upswings , we advocate shorting 2w (1%) OTM put option (position seems good even if the underlying spot goes either sideways or spikes mildly), simultaneously, go long in 2 lots of long in 2m ATM -0.49 vega put options.

The rationale for PRBS: Well, the traders tend to perceive these trades as a bear strategy, because it deploys more puts. But actually, it is a volatility strategy.

Hence, entering the position when implied volatility is high and anticipating for the inevitable adjustment is a wise thing, regardless of the direction of price movement. Based on volatility and time decay, the strategy is a “price neutral” approach to options, and one that makes a lot of sense.

Given the condition that, IVs keep rising and if GBPJPY spot keeps dipping, then the vega longs would add handsome option’s premiums to the price of such puts correspondingly, these derivatives instruments target further bearishness of this pair. Courtesy: sentrix

Currency Strength Index: FxWirePro's hourly GBP spot index is flashing -28 (which is mildly bearish), while hourly JPY spot index was at -17 (mildly bearish) while articulating (at 10:26 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex