UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data

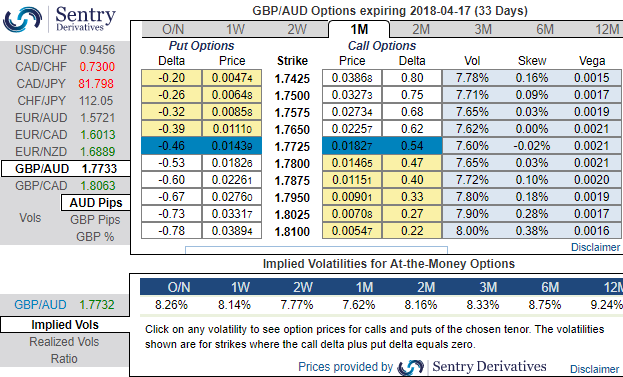

As for monetary policy, we remain to be convinced that a modest increase in UK rates over and above what is now priced (we expect 50bp this year) will be a game-changer for GBP. Growth may have improved in the UK but the country is still a clear laggard within G10 and monetary tightening is merely reducing the highly negative level of real UK rates. The Brexit vote may not have reduced the current account deficit to a more normal level notwithstanding the collapse in GBP (the deficit is currently averaging 4.5% of GDP), but it has led to a collapse in long-term capital inflows and so presents the UK with short-term financing requirement of around 5.5% of GDP. Capital inflows of this scale can’t be assured with real policy rates still below -2%.

Nevertheless, the modest acceleration in UK growth to around 2% doubtless contributed to the reversal of speculative positioning in GBP from heavily short to heavily long (more so CTAs than macro investors we believe) as it led to a firming up of UK rate expectations (one and a half hikes are now priced for the end of 2018, three and a half by end-2020) and the promotion of GBP to the vanguard of currencies where central banks are in the early stages of policy normalisation.

Well, all these macros standpoints could propel GBPAUD either side but more downswings potential.

Consequently, in the prevailing puzzled environment, you could observe that the momentary bulls of GBPAUD struggle to break and sustain above stiff resistance of 1.7928 levels, currently trading in non-directly to signal some bearish pressures. We advocate hedging strategy as stated below with cost-effectiveness that could hedge regardless of the swings on either side.

Hedging Framework:

3-Way Options straddle versus Call

Spread ratio: (Long 1: Long 1: Short 1)

The execution: Initiate long in GBPAUD 1M at the money -0.49 delta put, long 1M at the money +0.51 delta call and simultaneously, short theta in 1w (1%) out of the money call with positive theta or closer to zero.Theta is positive; time decay is bad for a buyer, but good for an option writer.

The Vega of a short (sell) option position is negative and an increasing IV is bad. Please be noted that the 1w IVs are just shy above 8.14%, whereas OTM calls of this tenor have been crazily overpriced above 25.85% more than NPV, hence, we foresee writing such exorbitant calls are beneficial as there exists the disparity between IVs and option pricing.

Hence, we encourage vega longs and short thetas in the non-directional trending pair but slightly favors bearish strategy as the vega signifies the sensitivity of an option’s value owing to a shift in volatility. It is usually expressed as the change in premium value per 1% change in implied volatility.

Currency Strength Index: FxWirePro's hourly GBP spot index has turned into 20 (which is neutral), while hourly AUD spot index was at shy above -96 (bearish) while articulating (at 10:14 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: