BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks

RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

Brazil’s long-awaited exit from recession took a step back this week, with a disappointing set of August activity data leading us to lower the growth projection for Q3’16 even though we still see a tepid recovery starting this quarter. At the same time, COPOM began its easing cycle this week but did so with a less-than-expected 25bp cut and adopted a more hawkish tone in the post-meeting statement.

The committee conditioned the pace of future cuts on the implementation of fiscal measures and the behavior of cyclically sensitive services sector prices. As we do not foresee an immediate improvement on these fronts, we moved our November call to a25bp cut (from50bp).

However, we see an increase in the pace of cuts after Congress finalizes the approval of the spending cap bill and makes progress on pension reform. We now anticipate that the CB may cumulate 300bp easing by mid-2017.

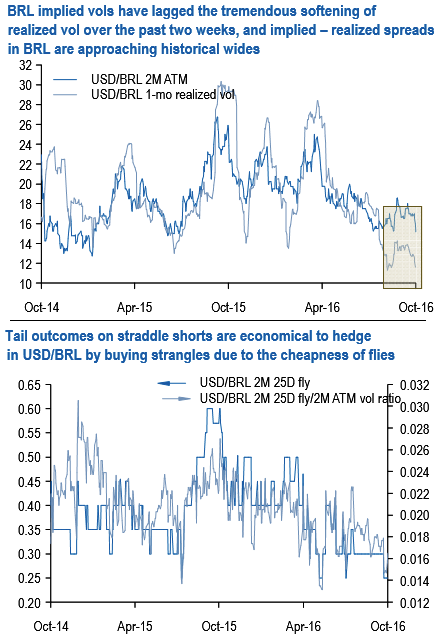

There are a few gamma shorts as convincing as BRL at present. USDBRL implied –realized vol spreads are stunningly wide (4w ATM – 4w hourly realized vol in excess of 7 % pts., 4.5 pts. if using close-to-close WMR measurements), and the leak lower in implied vols, even accounting for this week’s intense sell-off, has severely lagged the catastrophic decline in realized vol this month (see above chart).

The latter is due only in small part to the beta effect of the global compression in FX vol towards YTD lows; there is a larger, more important idiosyncratic component to the real narrative in that spot ranges have shrunk in the tug of war between attractive Brazilian real rates that have continued to fuel solid FDI and equity inflows and a still inexpensive currency, versus a considerably priced-in macro-recovery story, expectations of BCB rate cuts and still-extant fiscal uncertainty.

The new piece of information this week was that monetary easing that got underway this week is unlikely to derail the currency, judging by BRL’s positive response to a hawkish-sounding COPOM message (Hold BRL longs as the easing cycle kicked off with a ‘hawkish’ tone).

A slow grind lower in USDBRL towards 3.10 from here is likely to pressure front-end vols materially lower to reflect the exorbitant decay cost of owning options, and we sell delta-hedged 2M straddles to participate in the vol crunch.

For investors who would rather avoid the hassle of delta hedging and sell vol in management-lite capped loss format, we propose either (a) short straddle vs. long strangle spreads or (b) double no-touches. Both structures benefit from depressed levels of vol flies (see above chart) that render owning wings to eliminate tail losses of selling ATM vol an economical proposition.