How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

Leveraged funds were net buyers of USD for the fifth consecutive week, keeping the DXY Index firm. USD buying was largely broad-based, except against the yen. EM currencies saw net selling by both leveraged funds and asset managers. Given the downward pressure on EM asset prices from higher US bond yields, a stronger USD and rising oil prices, the positioning changes within the three EM currencies were fairly muted.

Asian currencies have taken a beating over the past few weeks, the entire complex initially weakening alongside a generalized upturn in the dollar and then the higher-yielding (INR, IDR) subset unraveling more rapidly in the last few days.

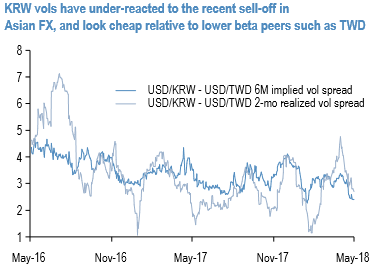

Front-end vols have crept higher to varying degrees across the board since mid-April, with one exception: USDKRW.

Arguably, a combination of Korea’s large current account surplus, positive sentiment surrounding North Korean de-nuclearization talks and potential central bank smoothing has insulated the currency from the regional malaise. It is also true that sizeable net equity outflows from the Korean equity market in 1Q’18 may have left the won less vulnerable to Q2’s 5% SPX drawdown.

Still, it is odd for implied vols in a high-beta currency like KRW to decouple so starkly from the regional trend at a time when the flow backdrop is similar in equity- sensitive peers like TWD, and considering upcoming trade-related event risks in the form of additional US tariff and tech/IP related announcements later in the month that can have ramifications for the entire North Asian tech supply chain.

Owning KRW vol standalone can be a painful proposition however if history is any guide, and the unpredictable longevity of this year’s 1060-1100 range looms as a realized vol drag on short-dated options.

Hence the need to pair KRW vega longs in mid-curve-to-long expiries with those in CNH and TWD where both implied and realized vols are less supportive (refer above chart).

Of the two, our bias is to choose TWD over CNH given that China is the epicenter of the trade dispute with the US and there are probably still greater residual directional long positions in CNH than TWD that could come in for liquidation should trade actions surprise negatively in coming weeks; if the 2015/16 China stress template is any guide, spec positions in USDTWD might even have flipped from short to long over the past few weeks as investors overlaid a positive carry hedge atop carry-friendly longs in CNH, implying potentially less deleveraging pain/realized vol for TWD if the entire North Asian FX bloc were to come in for sale.

We view the risk/equity beta differential between KRW (higher) and TWD (lower) as a positive for the trade that biases the vol spread wider in broad market stress. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is flashing at 84 levels (which is bullish) while articulating at (12:14 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: