Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

In many respects, we feel EM Asia FX is stuck between a rock and a hard place as we enter 2020. The bullish scenario is one in which we see a Phase I US-China trade deal, which drives USDCNH back below 7.00 and boosts sentiment, whilst the cumulative action of the G2 central banks aids a capex rebound and drives a turnaround in external demand for the region. However, our economists only expect a bounded lift in global capex, as we are late in the cycle and supply chains within the region have already started to shift.

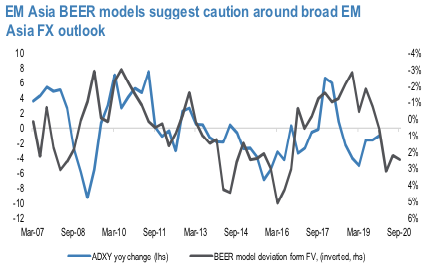

Moreover, current levels of the ADXY are already consistent with EM Asia export growth returning to positive territory. Hence, some ‘good news’ is already priced in. This viewpoint is supported by our BEER model metrics, which suggest EM Asia FX sits slightly on the expensive side. This leaves us trading with a tactical rather than strategic bias. We look for CNH strength in Q1, so we take off our USDCNH call but maintain spreads and the EURCNH strangle. USDINR looks good risk/reward via options at current levels, particularly as seasonals are favorable.

The bullish scenario is one in which we see Phase I US-China trade deal, which drives USDCNH back below 7.00 and boosts sentiment, whilst the cumulative action of the G2 central banks aids a capex rebound and drives a turnaround in external demand for the region.

However, our economists only expect a bounded lift in global capex, as we are late in the cycle and supply chains within the region have already started to shift. Moreover, current levels of the ADXY are already consistent with EM Asia export growth returning to positive territory. Hence, some ‘good news’ is already priced in. This viewpoint is supported by our BEER model metrics, which suggest EM Asia FX sits slightly on the expensive side. If we push forward this valuation gap from the BEER models by 12 months it does a reasonable job of lining up with the turning points of the ADXY (refer above chart).

Equally, though, reduced tail risks for a sharp CNY depreciation, coupled with the prospect of sequential improvement in data momentum, leaves it difficult to position aggressively for Asian FX weakness. The EM Asia FRI feel sharply between mid-May to early October but has stabilized in the last 2 months and nudged higher.

On this basis, the recommendations are generally tactical rather than strategic. We maintain a short EURCNH 2M 7.55-7.90 strangle, as an expression of the range bound CNH outlook. Courtesy: JPM