With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation

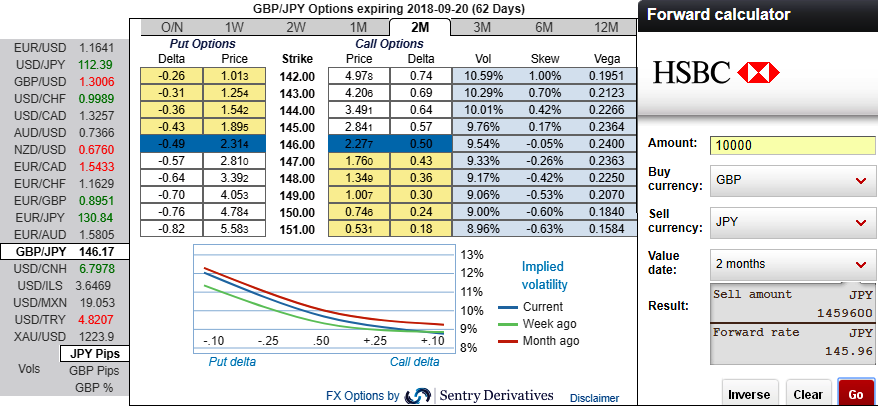

The valuation of financial derivative securities crucially depends on the market participants’ expectation of future volatility which is also known as implied volatility, and FX options are no exceptions. Hence, the essence of implied volatility arises as it often garners as much attention as the option price in option listings, and estimation of future volatility is a critical aspect of market research.

Before we proceed further, please be noted that the positively skewed IVs of 2m tenors signify the hedgers’ interests to bid OTM put strikes upto 142 levels (refer above nutshell evidencing IV skews). As you could observe GBPJPY forward rates across different tenors (refer above nutshell), these derivatives instruments indicate bearish targets of this pair.

Because the option pricing depends on future volatility, and it is quite impossible for anyone to ascertain accurate future volatility. Nevertheless, it is quite possible to calculate the marketplace’s expected future volatility using the option’s price itself which is known as implied volatility (IV). Options with a higher IV cost more. Well, this is quite intuitive owing to the higher likelihood of the underlying GBPJPY market ‘swinging’ in your favour. If IV increases and you are holding an option, this is good.

Most importantly, GBPJPY bears have resumed their business in the underlying spot FX prices. The pair has tumbled from the highs of 149.311 levels to the current 145.980 levels in just last 4-5 days. Thereby, prices have gone below 21-DMAs with strong downside momentum.

In this bearish scenario, put ratio back spreads have been advocated couple of days ago (to be precise on 27th June), wherein short leg has functioned since then as the underlying spot FX kept spiking exactly from 28th (refer above technical chart), we would like to uphold the longs in the same strategy on hedging grounds for now.

Both the speculators and hedgers who are interested in bearish risks are advised bidding 2m skews to optimally utilize Vega longs.

The execution: 2w (1%) OTM put option (position seems to be expired worthless as the underlying spot went upside), uphold longs in 2 lots of vega long in 2m ATM -0.49 delta put options. A move towards the ATM territory increases the Vega, Gamma and Delta which boosts premium.

The fresh Vega longs are encouraged for long-term hedging, more number of longs comprising of ATM instruments and ITM shorts in short-term would optimize the strategy.

Currency Strength Index: FxWirePro's hourly GBP spot index is inching towards -122 levels (which is bearish), while hourly JPY spot index was at 48 (bullish) while articulating (at 10:05 GMT). For more details on the index, please refer below weblink: