US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

Indian industrial production rose at 7.5% for Jan, inflation softens to 4.4% for February:

India's industrial production expanded by 7.5% YoY in January 2018, following a 7.1% gain in the previous month and beating market expectations of 6.7%. Manufacturing output growth picked up to 8.7% in January from 8.5% in December, and electricity production rose 7.6%, faster than 4.4% in the previous month. Meanwhile, mining output grew by only 0.1%, compared with 1.2% in the previous period.

Consumer prices in India increased 4.44% YoY in February of 2018, below 5.07% in January and market expectations of 4.8%. It is the lowest inflation rate in four months but above the 4% medium-term target of the central bank.

From last December (Dec-2017), USDINR has turned out to be slightly bearish. Our end-year forecast remains for USDINR to push above the 65.00 level.

While bearish INR risk scenarios are listed as follows:

1) Crude oil price gains accelerate;

2) The fiscal position deteriorates;

3) Exports continue to underperform

Bullish INR risk scenario: FII limits for local bonds are raised.

We maintain a modestly higher trajectory in terms of our USDINR forecast profile on a combination of a wider current account deficit this year, risks around fiscal slippage and underwhelming Indian export performance.

Positive carry and the RBI’s more than adequate FX reserves should keep any periods of INR weakness bounded. As we progress towards the end of Q1 we also tend to see seasonal strength in the currency. Some retracement in commodity prices, particularly in terms of energy, has also provided some relief in terms of the extent to which the current account balance is likely to deteriorate.

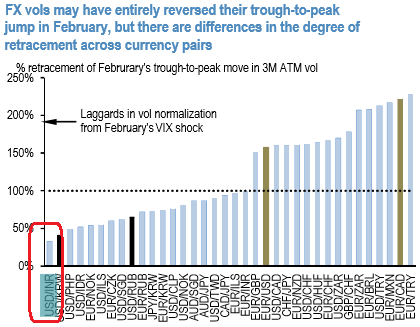

Trade tips: While low realized vol (least among the G20 FX universe, refer above chart) and technical support still indicates RKO put strategy, INR volatility stalls in the low vol bloc among the EM space (3m vol is trading below 6) but realized vol has remained constantly lower than implied vol since start 2016. The market is, therefore, pricing a premium not justified by the volatility of the FX rate.

This suggests selling volatility, and our USDINR bearish view combined with a strong technical support makes an RKO put attractive. While the skew oriented to the topside won’t provide an extra discount on the premium, such a positive skew indicates that market volatility should fall as the spot goes lower.

The rupee is strong on the back of custodial flows and upbeat GDP flashes. We continue to foresee USDINR to trade in a range of 63.25 - 65.953 in the months to come.

FxWirePro launches Absolute Return Managed Program. For more details, visit: