J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

Sterling has been the poorest performing among major currency space in the recent past as the market flipped the BoE from the vanguard to the rearguard of expected central bank policy normalization (the GBP NEER fell by nearly 3%).

The news flow was not universally negative –the government has moved to acknowledge the need for a lengthy Brexit transition that defers any economic adjustment for a number of years beyond the formal exit in 2019 – but weak cyclical developments are taking precedence.

In other words, the reality of a soft economy matters more for the near-term direction of the exchange rate than the expectation of a softer Brexit.

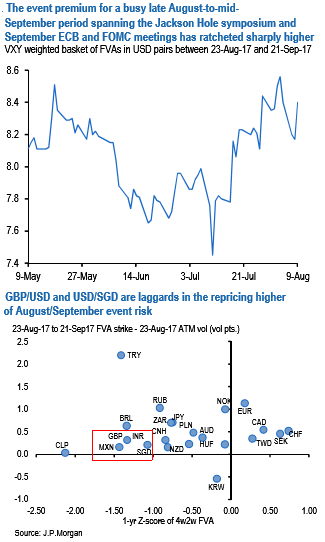

Event premium in the options market for the busy fall calendar has already ratcheted higher in recent weeks (refer above chart) and one straightforward play is to buy laggards in this repricing.

GBPUSD and USDSGD are two that fit the bill (refer above chart), with low nominal forward vols for the period covering the Jackson Hole symposium and the September ECB and Fed meetings (theoretical 23-Aug-17 to 21-Sep-17 FVA strike 7.5 for GBP, 5.0 for USDSGD) that are low by historical standards and price in only thin (< 0.5 vol) premium over pre-event dates.

Idiosyncratic vulnerabilities of the two currencies – GBP’s policy-related ones and SGD’s richness within the basket plus susceptibility to a Korea-driven regional deleveraging – are also supportive of vol ownership in these pairs. Source: JP Morgan