Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

We remain long Latam FX but mixed February performance makes us consider hedges. The Fed’s dovish tone and warming of China-US relations make us believe that a buy-on-dips strategy remains appropriate for now. FX valuations have become more concerning, and some optimism regarding reflationary dynamics (as shown by the disappointing China manufacturing PMI print) make us, on the other hand, prefer to maintain some defensive hedges as well.

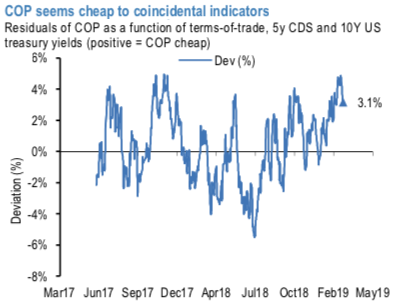

Stay long though despite some risks surfacing. The large rally in international oil prices YTD should continue to buoy COP, and we maintain that – despite COP’s strong performance - our valuation models continue to screen it as cheap. More specifically, normalized residuals of COP as a function of terms-of-trade, 10-year treasury yields, and the 5-year CDS, are showing the peso as 2.8% cheap (1.2 sigma, refer above chart).

Hence, we maintain our overall long Latam FX position in JPM’s GBI-EM portfolio (via BRL, COP and PEN) and our outright trades on hedging grounds: short USDARS 12m NDF (+3.0%), ahead of Brazil’s current account and FDI flow and Mexican retail sales data announcements we advise long BRLMXN (-3.2%), Buy 6M 25D BRL calls/JPY puts vs USD puts/BRL calls, equal vega.

Long USDCLP (+0.3%) and MXN puts with KO = 18.5. Buy 1M USDMXN vs. short USDBRL ATM, equal vega. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is at 21 (mildly bullish), EUR is at -100 (bearish) and JPY is flashing at 111 (bullish) while articulating (at 12:45 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex