China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

Despite a strong Christmas recovery in the US equity avenues, the broader market has largely snubbed the passage, with US yields and the USD remaining under pressure, amid such market sentiment, we emphasize on a RV implementation in the FX Vol space that efficiently eases tactical VIX declining slope over the next few weeks. The past few weeks were depicted by the tension on Equity markets, which nonetheless on average failed to propagate materially to the FX space (including EM), exhibiting a similar behaviour to the one from February.

Still, with a VIX at 21, having reached a post-February maximum of 25 two months ago, it is tempting to consider opportunities in the FX vol space for playing a further decline in the VIX (it remains 75% higher than the early October levels).

As the JPM’s equity derivatives crew projects a decline of the US Equity vol from current elevated levels in 2019, several factors also point to a short-term relief in market stress, amongst which increased expectations of a short- term easing in US/China trade tensions, more conciliatory tones in the Italy-EU dialogue regarding fiscal budget, and Theresa May’s confidence vote win earlier this week that possibly reduces the chances of a hard-Brexit.

While the structural factors supporting our strategic view that FX Vols are poised to rise over 2019 remain intact, the recent softening in the Fed stance is lending a helpful hand in relieving the recent downbeat sentiment pressures. With the holidays just around the corner, FX vol (VXY-GL down almost 0.5pts since the early Dec high) is on track to get a breather.

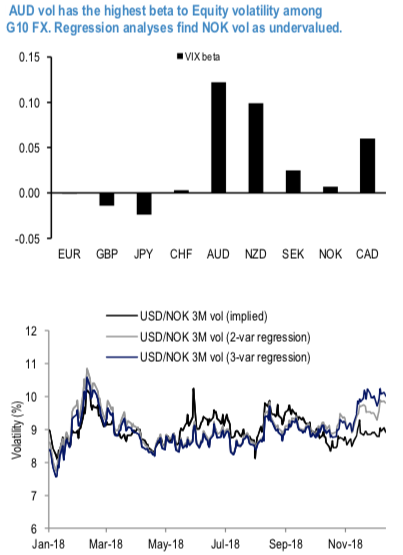

The abovechart displays the VIX-beta for DM FX vols (against the USD), in a 2-dimensional regression (with data since 2005) using also the VXY vol index as a regressor. Based on the chart, we note that AUD is the G10 FX volatility showing the highest sensitivity to the VIX, a specific which clearly manifested itself in early December. Investors interested in participating in a calmer year-end could consider tactically selling AUD vol for playing a lower VIX level over the next few weeks. Based on the same analysis, NOK vol is one of the least exposed to moves in the VIX.

Given the sensitivity of the currency to Oil prices, in the bottom chart (zooming on 2018 data) we compare USDNOK implied vol with two fair value regressions, one using the two factors described above, one incorporating Oil volatility as a third regressor. NOK volatility is undervalued in both (2- and 3-factor) regressions by around 1vol, having failed to react to a sharp rise in Oil volatility (to which it is positively exposed) in early November. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index has flashed at 37 (which is mildly bullish), while hourly EUR spot index has shown -31 (mildly bearish), while articulating at 10:09 GMT.

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex