Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch

The GBP forecasts are unchanged from the 2018 Outlook, albeit the risk bias is upgraded to positive as subsequent developments have been constructive on balance. In particular, favorable progress on Brexit has overshadowed marginally discouraging macroeconomic trends as the UK economy risks being eclipsed by an increasingly powerful global uptrend. The forecast essentially assumes that GBP's trade-weighted value will continue to drift within the sloppy 10% range that has prevailed since the Brexit vote. But this masks a rather more divergent pairwise performance as we expect GBP to weaken by a few percent vs EUR to 0.92 by year-end but to consolidate against a moderately weaker USD in the mid-1.30s and plummeted against yen upto 150.194 levels.

Brexit continues to dominate GBP, which is not unreasonable as there is a risk premium of between 10% (cyclical) and 15% (structural) for the long-term consequences of Brexit.

On the flip side, the latest development of JPY that caught market attention was its appreciation upon the BoJ’s announcement to decrease purchases of super-long bonds on January 9.

Technically, GBPJPY has been edgy at 152.121 – 153.600 levels ever since the occurrence of hanging man pattern candle which is bearish in nature, we anchor the prevailing bearish stance of is backed by both leading oscillators, one can think of short hedges in this pair only for the medium-term basis. For more readings, refer our technical section.

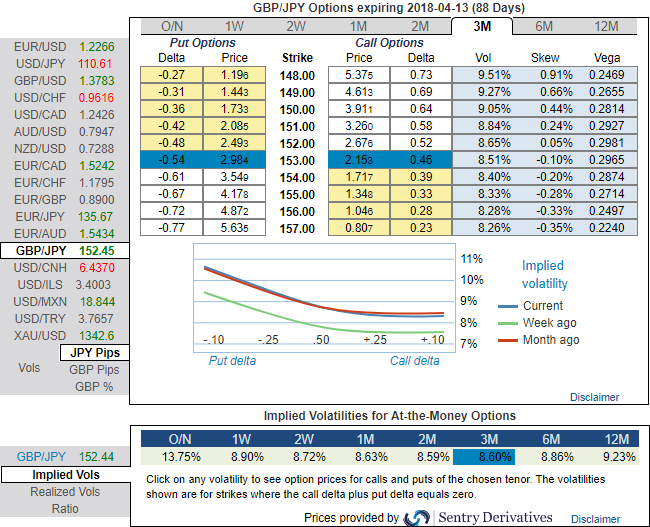

OTC outlook and Hedging Perspectives (GBPJPY):

Please be noted that the positively skewed IVs of GBPJPY of 3m tenors signify the hedgers’ interests in OTM put strikes (upto 148 levels) and isn’t this a luring factor for a shrewd bear. While 3m IVs of ATM contracts are trending above 8.6% which is the quite suitable conducive ATM put longs in diagonal put ratio spread that has been earlier advocated.

Because the higher IVs with well-adjusted positive skewness signify the hedgers’ interest for both OTM call/put strikes. In usual circumstances, long option position needs higher IVs for significant change in vega. Hence, we capitalize on buzzing IVs in 3m tenor for long leg and improve odds on options below strategy.

With this interpretation, we reiterate one can judge whether the options with a higher IV cost more. This is intuitive due to the higher likelihood of the market ‘swinging’ in your favor. If IV increases and you are holding an option, this is good.

The aggressive volatility investors want to capture GBP should consider buying ATM put instruments and/or being long of the smile convexity, against ATM volatility. Thus, ATM strikes are perceived to be more conducive than the OTMs.

Further GBPJPY upswings and/or weakness suggest building a directional strategies and volatility patterns at the same time.

In order to mitigate downside risks and keep them on the check, we advocate adding longs in 2 lots of ATM -0.49 delta puts of 3m tenor while writing 1 lot of 2% OTM put of 1m tenor.

Contemplating IV skewness and ongoing technical trend, we foresee the value of ATM options would likely rise significantly as the IVs seem to be favoring long legs of ATM strikes.

Currency Strength Index: FxWirePro's hourly GBP spot index is flashing 87 (which is bullish), while hourly JPY spot index was at -82 (which is bearish) while articulating (at 11:35 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: