Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman

Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand

Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Australian Household Spending Rebounds Strongly in May as Travel and Dining Drive Consumer Growth

Australian Household Spending Rebounds Strongly in May as Travel and Dining Drive Consumer Growth  Oil Prices Drop as Strait of Hormuz Shipping Recovers

Oil Prices Drop as Strait of Hormuz Shipping Recovers  South Korea’s KOSPI Rebounds as Samsung and SK Hynix Lead Tech Stock Recovery

South Korea’s KOSPI Rebounds as Samsung and SK Hynix Lead Tech Stock Recovery  U.S. Dollar Reaches One-Year High as Tech Sell-Off and Fed Rate Hike Expectations Support Demand

U.S. Dollar Reaches One-Year High as Tech Sell-Off and Fed Rate Hike Expectations Support Demand  Australia Inflation Cools in May, But Core CPI Keeps RBA Rate Hike Risks Alive

Australia Inflation Cools in May, But Core CPI Keeps RBA Rate Hike Risks Alive  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Drops Below $4,000 as Strong US Dollar and Fed Rate Hike Expectations Pressure Bullion

Gold Drops Below $4,000 as Strong US Dollar and Fed Rate Hike Expectations Pressure Bullion  Asian Markets Rally as Micron and Qualcomm AI Outlook Lifts Global Tech Stocks

Asian Markets Rally as Micron and Qualcomm AI Outlook Lifts Global Tech Stocks  US Dollar Climbs to One-Year High as Fed Rate Hike Expectations Surge

US Dollar Climbs to One-Year High as Fed Rate Hike Expectations Surge  White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response

White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

Over the weekend, the Bank of Canada cut its key interest rate by another 50 bp, after it had lowered its key interest rate from 1.75% to 1.25% at its regular meeting. The BoC also said that it was ready to take further steps if necessary.

Not only does the impact of the covid-19 pandemic pose significant downside risks to the Canadian economy, but also the sharp drop in oil prices is likely to weigh on the Canadian economy. The coronavirus has not yet spread so strongly in Canada. But experience shows that this can change quickly. The pandemic is certainly noticeable. Tourism, retail, restaurants, entertainment: There are already significant cutbacks. Now the border is also being closed.

In view of the high level of uncertainty, it is therefore understandable that the central bank has confirmed its willingness to act if necessary. At the moment, it looks as if this will actually become necessary, so we expect a further interest rate cut at the latest at the regular meeting on April 15. The CAD should therefore remain under depreciation pressure and USDCAD should remain above 1.40.

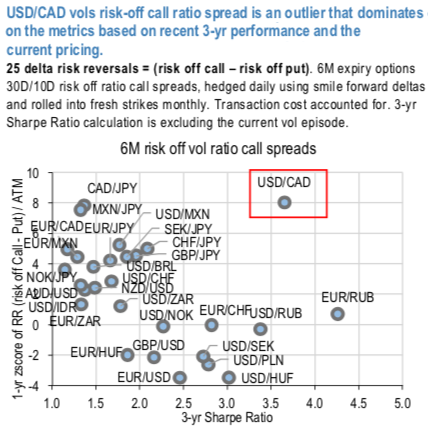

While the market sentiment has been driving strictly defensive positioning we think that it is prudent to keep an eye on historic skew dislocations their theta-scalping via risk off ratio spreads (delta-hedged). Those are a class of structures that can efficiently monetize excessive risk premia in vol smiles. While ratios can be struck for both calls and puts, the recent vol episode pushed the pricing of risk of OTM strikes into uncharted territory and made of particular interest the structures where the short notional is placed on the “risk-off” side, i.e. selling risk-reversals. While such structures are quicker in collecting premium, exposure to left tail is notable.

USDCAD vols risk-off call ratio spread is an outlier that dominates (refer above chart) where currency pairs are screened based on 3 year Sharpe (a medium term performance horizon) of risk off ratio vol spread structures and 1-y zscore of skew / ATM vol ratio.

3M USDCAD delta-hedged ATM/25D call spread @9.8/10.3indic vs 12.7ch, equal notionals to keep the structure net long vega. Courtesy: JPM & Commerzbank