Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

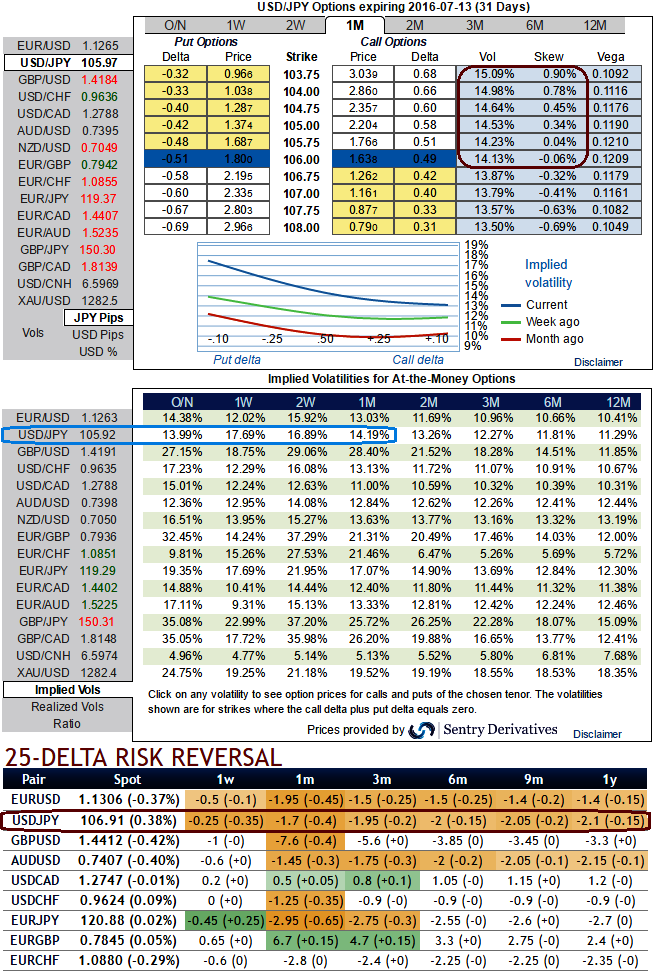

Amid various central banks’ monetary policy season, this week include the US FOMC, Bank of England, Bank of Japan and Swiss National Bank.

Most attention is likely to be on the FOMC, which is most likely to leave policy rates on hold, with Chair Yellen set to communicate on the risks to the economic and policy outlook.

The Fed meets this week (June 14/15) but that is unlikely to be the focus with Brexit looming.

OTC updates:

As you can probably observe, options of OTM put strikes evidence higher skews with higher vols.

The current ATM IVs are trending above at 17.69% ahead of above mentioned central banks events.

While delta risk reversal of this pair signals more bearish pressures in long run by flashing negative RR numbers.

Why do we think USDJPY sensing pressures for downside risks: The delta risk reversals evidence the difference in volatility on various strikes, and therefore the price difference between puts and calls on the most liquid out-of-the-money (OTM) options quoted on the OTC market.

Since these FX options risk reversals take volatility analysis one step further, practise them not to predict market conditions but as a gauge of sentiments on a specific currency pair.

That is why while formulating hedging strategy, in FX options weekly forecasts, we use RR to gauge trends and shifts in trends for major currency pairs.

Yet we have found it is a bit more difficult to use the absolute Risk Reversal number in creating set strategies, as different dynamics across currency pairs complicates standardization of strategy rules.

Although the Fed will likely to remain on the sidelines on March 16th, the improving domestic backdrop supports our view that the Fed will continue on with its gradual tightening cycle in June.

We think current macro situations lead the fed to almost defer policy actions to June meeting, but manipulative statements on monetary policy outcome may keep USDJPY at stake.

On the other hand, we can very much empathize with this Yen against the dollar to gain slightly at least in the short run (let's say next 2 months or so) with an anticipation of Fed may continue to hold on its rate stance until Q1'16 considering global economic slowdown.

Since implied volatility is inching higher when risk reversals are higher comparatively to 1M expiries that is a good scenario for option holders in next 1-3 months, go long in 2 lots of ATM and OTM put with longer expiry (per say 2M expiries) and simultaneously short ITM puts of shorter expiries (preferably 1W tenors) with positive theta values.