Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Open-Source AI Models Gain Ground as Enterprises Seek Lower-Cost Alternatives, Citi Says

Open-Source AI Models Gain Ground as Enterprises Seek Lower-Cost Alternatives, Citi Says  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

It is observed that the Japanese retail investors likely to surge foreign stock investments through investment trusts especially between May and July as we saw in the past two years. It is also expected that the USDJPY to rebound in 2Q a bit.

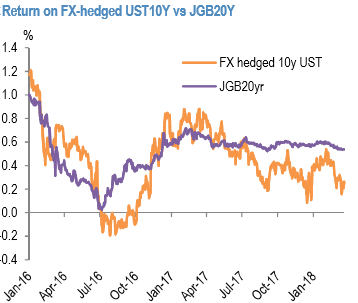

While the U.S. short-term interest rates have risen sharply, meaning that returns on FX-hedged U.S. bond investments are falling (refer 1st chart).

The US 10yr treasury yield rose from 2.77% to 2.84%, 2yr yields from 2.30% to 2.35%. Fed fund futures yields firmed to price the next rate hike in June as a 90% chance.

Given that U.S. long-term rates are relatively high and that the USDJPY rate is currently below the lower end of the CY’2017 range, life insurers could reduce the FX hedge ratio on U.S. bond holdings and a greater portion of their new overseas bond investing could be un-hedged. It would cause JPY sales.

Life insurers currently own a total of around ¥85 trillion in overseas bonds, and we estimate the ratio of FX-hedged overseas bonds to be around 70%.

Since reducing the ratio of FX-hedged bonds by 1% means selling over ¥800 billion worth of JPY, the impact cannot be ignored.

Separately, although returns on FX-hedged U.S. bond investments are diminishing, the returns on FX-hedged European bonds are relatively high (refer 2nd chart). While this would have no impact on the JPY market, we think FX hedged overseas bond investing by Japanese investors will probably shift away from U.S. bonds and toward European bonds.

Over the four months spanning October 2017 to January 2018, domestic investors were net sellers of U.S. bonds by ¥4.5 trillion and net buyers of European bonds by ¥2.8 trillion.

It seemed that in the recent times as if USDJPY was displaying exchange rate moves that correlated with the risk-on/-off news flow. But as soon as one takes a look at exchange rate moves of the second typical safe-haven currency, the Swiss franc, this does not really work. I fear the correlation structure of the exchange rates cannot be explained with simple, mono-causal stories such as risk-on/risk-off at present. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: