AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Aside from the overarching issue of Brexit, the GBP forecast also needs to take account of the deterioration in the UK’s contemporaneous economic performance as evidenced already in the halving of growth in 1Q17 vs 4Q18 (1.2% versus 2.7%). This is perhaps something which GBP bulls are now overlooking, in part because the economy defied the pessimists in such impressive fashion in the first six months following the vote.

Still, whereas investors may be able to live with the prospect of Brexit if the consequences of this won’t be felt for perhaps three-four years, it is not clear to us that GBP will be able to appreciate on a sustainable basis now that growth and interest rate differentials are finally starting to shift against the UK (growth differentials versus the Euro area and interest rate differentials versus the US).

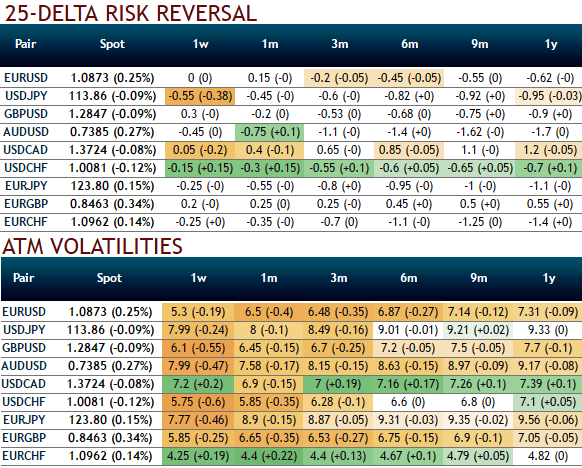

As you could spot out the implied volatilities of GBPUSD ATM contracts from the nutshell evidencing IVs the contract of this underlying pair of all expiries have been the least among G10 currency segment and the range bounded trend is foreseen in near future but little weakness on weekly charts is puzzling this pair to drag southward targets but very much within above-stated range.

As a result, we recommend below option strategies using right options, thereby, one can benefit from certain returns.

Naked Strangle Shorting:

Short 1W OTM put (1.5% strike difference referring lower cap) and short OTM call simultaneously of the same expiry (1% strike referring upper cap) (we reiterate, preferably short term for maturity is desired).

Overview: Slightly bearish in short term but sideways in the medium term.

Timeframe: 7 to 10 days

Alternatively, one can also prefer iron condor on the same lower IV circumstances. To execute the strategy, the options trader buys a lower strike OTM put, sells a middle strike ATM put, sells a middle strike at-the-money call and buys another higher strike OTM call. This results in a net credit to put on the trade.

For all of the intense focus on the Brexit process, GBP’s fate over the coming 12 months may ultimately be determined by more parochial, and in all likelihood negative, cyclical factors.

Weighing all of these considerations, we lower the 1Y forecast for EURGBP 0.91 to 0.88 and lift the 1Y forecast for GBPUSD from 1.26 to 1.31 (remember that we forecast a bounce in EURUSD to 1.15 on a 1Y window).