European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

In December 2016, the dollar reached its third and smallest significant peak (in real terms) since 1980. The question of cheap short dollar hedges has frequently arisen in the recent past. In our latest write-ups, it was screened for highly levered standalone USD calls (2M 5:1 one-touches) that offered the highest ex-ante odds of paying out in the event of a dollar reversal, and surmised that Gold, ZAR and AUD puts/USD calls offered the most value for hedgers; this section extends the dollar hedging question here to relative value constructs.

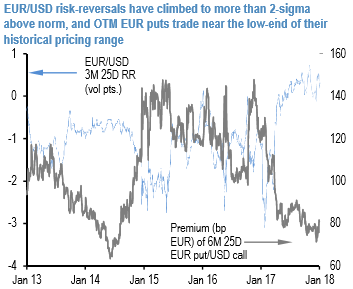

1. Long EUR puts/USD calls vs. short EUR calls/CEE and Scandinavia puts: A notable by product of the ferocious dollar sell-off of the past few weeks is that risk reversals have re-priced sharply away from USD calls towards USD puts, and currently trade close to zero, or even in favor of USD puts in some G10 majors. EURUSD is one of the most extreme examples of this dynamic, where RR/ATM ratios have risen to 2-sigma above the norm (3M 25D r/r +0.3; refer above chart). The rare surface configuration of a vol discount on OTM EUR puts, coupled with positive forward points carry on bearish Euro bets motivates cheap option protection for long cash positions. The clean hedge is to buy outright OTM EUR puts/USD calls that trade near the low end of their historical price scale (refer above chart).

2. Long USD calls/CNH puts vs. short EUR calls/CNH puts: Short USDCNH is a well subscribed to directional view, in part as a positive carry beta expression of dollar weakness / Euro strength with solid growth differential underpinnings, and partly for alpha reasons related to trade friction related official tolerance for a stronger Renminbi.

Much like EURUSD, USDCNH risk reversals have compressed sharply amid the 4.5% drop in the spot since December –1M 25D skews even flipped briefly for USD puts at one stage – and are depressed relative to ATM vols and implied yields in forwards. Unlike with the Euro, however, owning USD calls/CNH puts standalone as a dollar reversal hedge is expensive on account of the negative carry in points despite cheap vols.

For more details on the index, please refer below weblink: