JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations

Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  South Korea Warns Won Is Undervalued, Boosts FX Coordination With Japan

South Korea Warns Won Is Undervalued, Boosts FX Coordination With Japan  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes

Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms  Asian Stocks Slide as Chip Shares Tumble Ahead of Key U.S. Jobs Report

Asian Stocks Slide as Chip Shares Tumble Ahead of Key U.S. Jobs Report

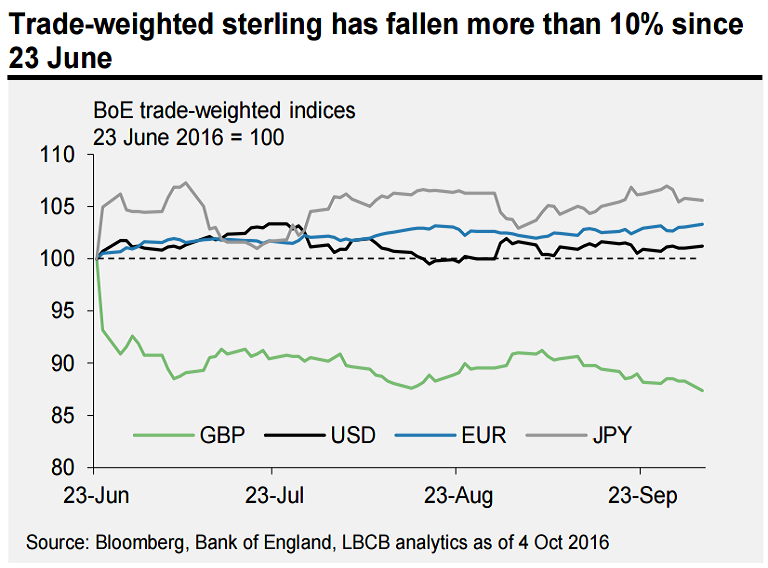

UK Prime Minister Theresa May's announcement to invoke article 50 by March 2017 at the latest, thus starting official exit negotiations has put considerable pressure on the Sterling. Markets are seeing an increased probability of what is widely reported in the media as ‘hard Brexit’. The pound sterling continues to decline, has not recovered after the June referendum vote despite incoming data showing strong resilience.

May said she wanted to give “British companies the maximum freedom to trade and operate in the single market”, but not at the expense of allowing free movement or accepting the jurisdiction of judges in Luxembourg. The European Union, however, sees the free movement of workers and oversight of a single court as indispensable pillars of a common market.

Limiting the freedom of movement is unlikely without May having to accept notable restrictions when it comes to accessing the single market. This is likely to lead to considerable economic effects, dent attractiveness of GBP investments and hence increases fears of a “hard” Brexit. Sterling is likely to remain under pressure until an amicable agreement can be reached in this matter.

Data released earlier today showed UK construction PMI jumped to 52.3 points in September, substantially above and building on to 49.2 in the previous month. The data surprised economists who had forecasted a reading of 49.0. Manufacturing sector activity also surprised the markets to the upside, extending further into the expansion territory, as markets shrug Brexit-related concerns. Data released on Monday showed that UK Markit/CIPS manufacturing Purchasing Managers’ Index (PMI) rose to 55.4 from 53.4 in August, beating expectations for a reading of 52.1.

Upbeat data did little to help improve sentiment around the GBP. Cable broke the low made on July 7th 2016 (Brexit low) and made a fresh record low of 1.2736. EUR/GBP hit fresh multi-year highs at 0.8765. The speculative market positions remain stretched to historical extremes: net speculative shorts are nearly 2 standard deviations above the historical mean. The consensus forecast for the GBP/USD at year-end is 1.27.