U.S. Dollar Reaches One-Year High as Tech Sell-Off and Fed Rate Hike Expectations Support Demand

U.S. Dollar Reaches One-Year High as Tech Sell-Off and Fed Rate Hike Expectations Support Demand  Gold Prices Fall Below $4,000 as Strong Dollar, Fed Rate Hike Bets Weigh on Bullion

Gold Prices Fall Below $4,000 as Strong Dollar, Fed Rate Hike Bets Weigh on Bullion  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Wall Street Ends Lower as AI Stocks Drag Markets, Fed Rate Outlook Shifts

Wall Street Ends Lower as AI Stocks Drag Markets, Fed Rate Outlook Shifts  Asian Currencies Trade Mixed as Yen Hovers Near 40-Year Low, Dollar Holds Firm on Fed Outlook

Asian Currencies Trade Mixed as Yen Hovers Near 40-Year Low, Dollar Holds Firm on Fed Outlook  Gold Price Ends Lower for Fourth Week Despite Rebound as Fed Rate Hike Bets Strengthen

Gold Price Ends Lower for Fourth Week Despite Rebound as Fed Rate Hike Bets Strengthen  SpaceX Eyes Starlink Mobile Phone Service to Challenge Verizon, AT&T, and T-Mobile

SpaceX Eyes Starlink Mobile Phone Service to Challenge Verizon, AT&T, and T-Mobile  Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman

Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman  White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response

White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response  Australian Household Spending Rebounds Strongly in May as Travel and Dining Drive Consumer Growth

Australian Household Spending Rebounds Strongly in May as Travel and Dining Drive Consumer Growth  Wall Street Ends Mixed as Micron Surges, Apple Drops After Price Hikes

Wall Street Ends Mixed as Micron Surges, Apple Drops After Price Hikes

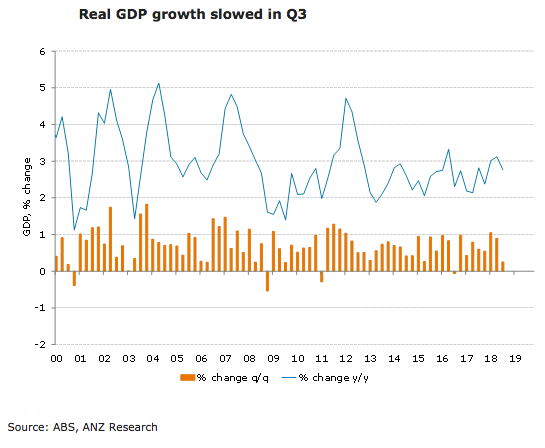

Australia’s gross domestic product for the third quarter of this year rose lower than market expectations, also down from the previous reading in the second quarter of this year. While public spending and net exports were strong contributors to growth, housing construction only eked out a small gain and consumption growth slowed significantly.

Underlining the softness in consumption was further weakness in wages growth. Persistently low wages growth raises the risk that household income growth will not pick up enough to offset the ongoing decline in house prices and support growth in consumer spending.

"In the near term, however, overall GDP growth is likely to hold up given the solid pipeline of public spending, business investment and exports," ANZ Research commented in its latest report.

GDP was up a modest 0.3 percent q/q in Q3, following a rise of 0.9 percent in Q2. Annual growth edged down to 2.8 percent from a downwardly revised 3.1 percent (previously 3.4 percent). The result is likely to be weaker than the RBA expected, with a step up to 1.2 percent q/q in Q4 required to achieve the forecast of 3-1/2 percent by end year published in the November Statement on Monetary Policy.

There were a few downside surprises in the release. In particular, business investment was weaker than was expected, with a sharp fall in mining investment (-7.5 percent q/q) – much weaker than the 2.7 percent decline reported in the capex survey – driving the fall.

Small business profits (-1.3 percent) were also weaker than the Business Indicators Release suggested, likely driven down by falling farm incomes. Household consumption growth (+0.3 percent q/q) was also lower than our forecasts, while wages growth was another area of disappointment.

The persistent weakness in wages growth is surprising. The GDP measure of non-farm average wages rose just 0.2 percent q/q following a 0.1 percent rise in Q1. Annual growth is now at just 1.2 percent, and slowing. Once again, this is a disappointing outcome, and suggests that the tighter labour market is putting very little pressure on labour costs.

"With house price weakness intensifying, wages slow to pick up and consumption softening, the outlook may not be so rosy. This suggests that it will still be some time before inflationary pressures lift, keeping the RBA on hold until well into 2020," the report further commented.