ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

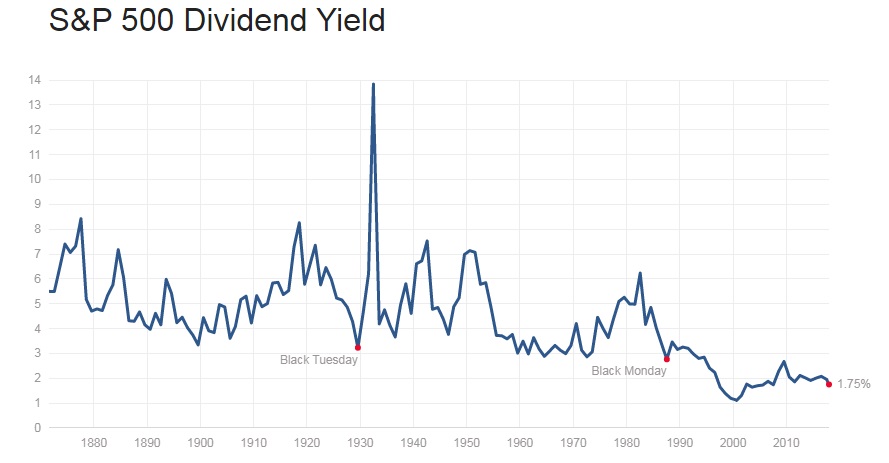

2017’s rally in the U.S. stocks is continuing well into 2018. However, some signs are emerging which suggests that stocks are becoming overvalued and a correction looks increasingly likely. In 2017, the U.S. benchmark stock index returned more than 19 percent and in 2018, they have returned 2.9 percent so far, which is quite remarkable. While the latest increase is being supported by the recent changes in the U.S. tax code, one indicator is strongly suggesting stock overvaluation despite the tax euphoria.

The above chart shows the historical S&P500 dividend yield. As of latest data, it has declined to 1.75 percent, the lowest level in more than a decade, while the recent rate hikes by the U.S. Federal Reserve has pushed the short-term rate (both1-year and 2-year) above the dividend yield. The dividend yield is widely used to calculate the future return from stocks.

As of today, the U.S. 1-year treasury is returning about 1.78 percent, while the 2-year treasury is returning about 1.97 percent. A further spike in yields and rate hikes could bring about a major correction in the stocks.