US-Iran Ceasefire Under Pressure as Fresh Strait of Hormuz Clashes Shake Oil Markets

US-Iran Ceasefire Under Pressure as Fresh Strait of Hormuz Clashes Shake Oil Markets  Asian Currencies Slip as US Dollar Gains on Rising Iran Tensions and Awaited Jobs Data

Asian Currencies Slip as US Dollar Gains on Rising Iran Tensions and Awaited Jobs Data  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  European Stocks Fall as US-Iran Conflict Rekindles Energy Supply Fears

European Stocks Fall as US-Iran Conflict Rekindles Energy Supply Fears  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions  European Stocks Edge Higher as Iran-U.S. Peace Talks Boost Market Sentiment

European Stocks Edge Higher as Iran-U.S. Peace Talks Boost Market Sentiment  Gold Prices Hold Firm as Iran Tensions and Dollar Swings Drive Safe-Haven Demand

Gold Prices Hold Firm as Iran Tensions and Dollar Swings Drive Safe-Haven Demand  Trump-Xi Meeting 2026: U.S.-China Trade Tensions Escalate Ahead of Beijing Summit

Trump-Xi Meeting 2026: U.S.-China Trade Tensions Escalate Ahead of Beijing Summit  China Export Growth Surges in April as Global Buyers Rush to Secure Supplies

China Export Growth Surges in April as Global Buyers Rush to Secure Supplies  Iran-U.S. Peace Deal Near as Oil Prices Fall and Nuclear Disputes Persist

Iran-U.S. Peace Deal Near as Oil Prices Fall and Nuclear Disputes Persist  Russian LNG Shadow Fleet Expands Amid Arctic LNG 2 Sanctions

Russian LNG Shadow Fleet Expands Amid Arctic LNG 2 Sanctions

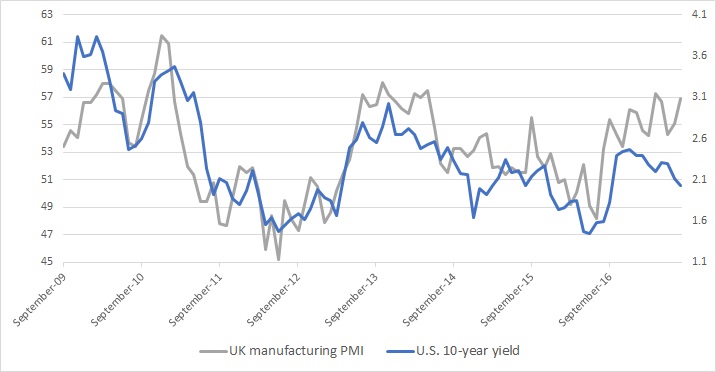

The above four charts show the relation between U.S. 10-year yields and manufacturing PMI numbers from the United States, Switzerland, Eurozone, and United Kingdom. We have chosen U.S treasury as a representative of global yield due to the importance of the U.S. dollar in the global financial system. Even if we had chosen 10-year yield from each region, the outcome wouldn’t be starkly different.

All four charts are showing the close relationship between the manufacturing PMI and 10-year yields, which is not surprising given the fact that central banks do not have much influence on the long term yields, unlike the short-term yields. Long-term yields like 10-years depend on the inflation outlook, state of the economy, savings glut etc.

All four charts have recently been flashing warning signs. A continuing divergence is quite visible for all four charts; extreme for Eurozone. It can be seen that while manufacturing PMI is moving higher, the 10-year treasury yields have been moving lower. For the United States, the divergence began last December and still continuing. For Eurozone, it began back in September 2015. For the UK, the divergence began in 2015, it closed somewhat last year but the gap started widening again since December. For Switzerland, the divergence began December last year and still growing.

While a divergence is n not an all new phenomenon, as can be seen in the chart of U.S. ISM manufacturing PMI and 10-year yields. Back in 2014, a divergence occurred. From March to October 2014, while PMI grew, U.S. treasury yield headed lower. But the divergence collapsed with a slowdown in the economy. So the real question is ‘what will happen this time around? Will yields move higher or will economy slow down?’