FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

After three hikes in 2017, the U.S. Federal Reserve forecasted four more rate hikes in 2018. FOMC has hiked thrice and the last hike is priced in December. In 2019, FOMC forecasted two more rate hikes. However, the actual number of hikes and the path forward would depend a lot on the actual inflation readings.

Why important?

- Fed’s dual mandate is price stability and maximum employment. The Unemployment rate has now reached 3.8 Percent in the US, which is the long-term unemployment level, consistent with the Fed’s dual mandate. That leaves inflation to be the most vital mandate for subsequent hikes.

- As inflation expectations increased, the fed projected four rate hikes until the end of 2019. The current Federal Funds rate is at 2.00-2.25 percent. Hence, the actual inflation would need to evolve in such a manner to warrant those hikes.

- As forecasted, the inflation numbers are proving to be a key determinant of exchange rate divergence among major economies in recent years.

Past trends –

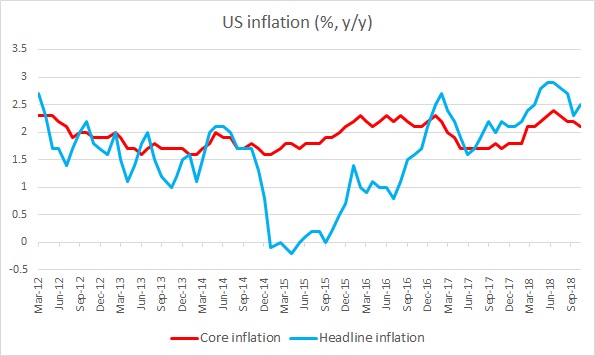

- After staying below FED’s 2 percent target, headline CPI fell to negative territory in the final quarter of 2014. In January CPI fell by -0.7 percent on monthly basis, mostly due to lower energy prices. Yearly CPI fell by -0.1 percent y/y in January.

- Yearly change in CPI has been minimal since then, growing about 0.04 percent per month.

- Yearly CPI growth was +0.7 percent in December 2015, the first sign of a comeback.

- In Mach 2016 it showed further signs of a bounce back, with 0.9 percent y/y. Consumer price index was up 1 percent in June 2016 and 0.8 percent in July on a yearly basis. In August it picked up further to 1.1 percent y/y. It rose again in September by 1.5 percent and by 1.6 percent in October. It rose further to 1.7 percent in November. 2016 ended with 2.1 percent y/y inflation. So, it 2017. But it picked up in 2018.

- It recently reached 2.9 percent y/y in July and declined to 2.7 percent y/y in August.

- Look at the above chart for greater clarity.

- In addition to that, core CPI has been showing remarkable resilience, monthly growth not falling below zero since February 2010. It ended the year 2016 with 2.2 percent growth in prices and ended 2017 with 1.8 percent growth in prices. Core CPI reached 2.2 percent in August.

Expectation today –

- CPI is expected to grow 0 percent m/m in November and rise by 2.2 percent on yearly basis.

- Core CPI is expected to grow at 2.2 percent on yearly basis.

- The data will be released at 13:30 GMT.

Impact –

- Further firming up of the consumer price index (CPI) is likely to boost the odds of rate hikes for 2018, as well as 2019. However, with the lower oil price, a higher level of CPI is a far-fetched idea.

- It is also likely to provide support to the dollar, which has been struggling lately. The dollar index, which is the value of the dollar against a basket of currencies, currently trading at 97.4, down 0.08 percent for the day so far.