Dollar Surges as Inflation Data Fuels Fed Rate Hike Expectations

Dollar Surges as Inflation Data Fuels Fed Rate Hike Expectations  Gold Prices Hold Steady as Investors Monitor U.S.-Iran Tensions and Trump-Xi Summit

Gold Prices Hold Steady as Investors Monitor U.S.-Iran Tensions and Trump-Xi Summit  US Stock Futures Slip as Iran Tensions and Hot Inflation Data Pressure Wall Street

US Stock Futures Slip as Iran Tensions and Hot Inflation Data Pressure Wall Street  Wall Street Futures Rise Ahead of Trump-Xi Summit as Tech Stocks Lead Market Rally

Wall Street Futures Rise Ahead of Trump-Xi Summit as Tech Stocks Lead Market Rally  S&P Global Revises Mexico Credit Outlook to Negative Amid Rising Debt Concerns

S&P Global Revises Mexico Credit Outlook to Negative Amid Rising Debt Concerns  U.S. Urges China to Help Curb Iran’s Actions in Gulf, Rubio Says

U.S. Urges China to Help Curb Iran’s Actions in Gulf, Rubio Says  AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says  Rubio Discusses Iran Crisis and Strait of Hormuz Disruptions With UK and Australia

Rubio Discusses Iran Crisis and Strait of Hormuz Disruptions With UK and Australia

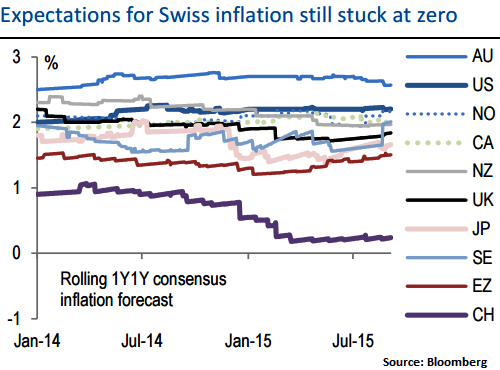

The driving factor behind our long-term CHF view is Switzerland's inflation outlook which will allow the SNB to keep its nominal rates lowest in the world. It has reported its CPI MoM numbers at 0.1% from previous -0.2%.

While its real rates are amongst the highest in G10, we have shown before those nominal rates are more important in driving spot FX returns. The above diagram shows updated 1Y1Y consensus expectations (year ahead inflation, 12 months out).

By 2016, Switzerland is expected to be the only G10 country with inflation still hugging zero. The SNB does not expect inflation to turn positive until early 2017 and it expects to keep rates at -0.75% throughout the forecast horizon. But the combination of previous CHF appreciation, lower commodity prices and slack in the economy all conspire to keep inflation soft and CHF slowly trending lower.

European rates are now expected an extension to ECB QE in Sept 2016 which should flatten the path for EUR/CHF next year.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Switzerland finally moves out of deflation zone

Tuesday, October 6, 2015 1:10 PM UTC

Editor's Picks

- Market Data

Most Popular