Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions

Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions  OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

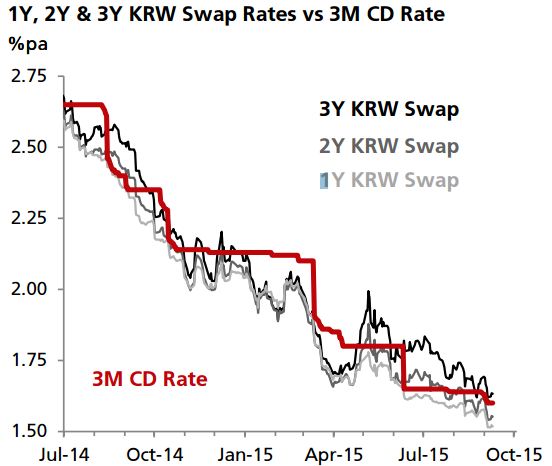

The market is pricing an outside chance of rate cuts within the next six months as sentiment on the Korean economy sours. The market is more dovish for the Bank of Korea (BoK) to keep the policy rate unchanged at 1.5% through to 3Q16.

Over the past two month, short-term KRW swaps (2Y and 3Y) have completely retraced the upmove seen in 2Q this year and are plumbing new lows. The renewed collapse in commodity prices and lackluster export demand are the two key reasons this development.

Speculation of rate cuts to prevent the KRW from being too strong versus peers was a key reason driving KRW swap rates lower. However, according to DBS Bank, this argument is no longer valid as the KRW has weakened significantly over the past few weeks, catching up with its Asian peers. Export competitiveness has become less of an issue. Moreover, with the domestic economy showing tentative signs of bottoming out, the market is likely to focus on domestic and external stability risks.

"In the absence of rate cuts, we think short-term KRW swap rates are biased modestly higher over the coming months," added DBS Bank.