Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

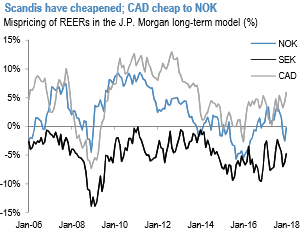

The largest G10 movers since our last publication in October were GBP and EUR (outperformed) while the underperformers were CAD and Scandis (unchanged vs USD). The dollar has weakened broadly versus all G10 currencies since then, weakening 1.3% in TWI terms.

Scandis have weakened and are now among the cheapest G10 currencies on this framework following the poor performance since October. Swedish Krone seems to be resilient and stable. The krone was hurt after the summer due to strong euro appreciation and a particularly dovish Riksbank communication. However, after testing and rejecting horizontal resistance at 10 in November 2016 and November 2017.

Norway and Sweden are experiencing strong growth but are at different stages of their cycles: Sweden’s expansion has decelerated, whereas Norway is playing catch-up. Meanwhile, Sweden’s housing market is probably a bigger risk than Norway’s. Real house prices have increased faster in Sweden, raising more financial stability risks and potentially a higher risk of a central bank policy mistake (the market has kept in mind the Riksbank’s dangerous tactic of ‘leaning against the wind’). Moreover, NOK rates have delivered decent carry, whereas SEK short rates are still anchored in negative territory.

Finally, NOK/SEK has likely formed a double-bottom just above parity, suggesting that the market is unwilling to go short the cross.

NOK has fallen down the ranks specifically since it hasn't kept up with the oil price increase. While NOK is not as mispriced as SEK, it is cheap relative to the other G10 petro FX, CAD (refer above chart).

The FX option prices are not priced in the unambiguously positive asymmetry of Swedish Krona spot outcomes. Prices of at-expiry digital (AED) options would be construed as probabilities of spot ending at or beyond strike thresholds at maturity, and are useful for studying the option-implied likelihood of spot outcomes.

One side-effect of the correction in EURUSD has been that PLN and SEK, both of which we like, have fallen further against the dollar than the euro has. That’s not a new pattern and points to heavy positioning, as many people bought ‘euro-alternatives’ rather than the real thing, earlier this year.

The starkly positive asymmetry of SEK spot outcomes is not reflected in option prices. Prices of at-expiry digital (AED) options can be interpreted as probabilities of spot ending at or beyond strike thresholds at maturity, and are useful for studying the option-implied likelihood of spot outcomes.

We favored buying zero-cost combinations of long EUR put/SEK call vs. short EUR call/SEK put digitals to position for an eventual normalization of Riksbank policy; we still maintain this position. At spot ref: 9.8415, 6M 9.7510 EUR put/SEK call vs 10.0320 EUR call/SEK put at-expiry digital risk-reversal has a net premium credit of 2.7% EUR (-5.2 /2.7 two-way indicative. assuming equal EUR notionals/leg). The short strike is above the YTD high, hence reasonable cushion against a backup on the spot.