Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  FxWirePro- Major Crypto levels and bias summary

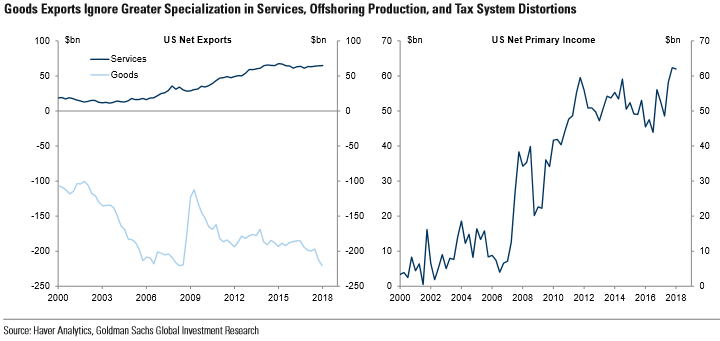

FxWirePro- Major Crypto levels and bias summary  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

Since our last monthly publication in May, the dollar has continued to strengthen. The bulk of USD strengthening has come against EM currencies, but performance has outperformed most currencies in G10 as well. Regional divergences in G10 reflect EM biases with Asia-linked and defensive currencies (AUD, CHF and NZD) outperforming vs. USD in the past month, but Euro area-linked currencies (EUR and SEK) weakening the most.

The RBA is scheduled its monetary policy meeting this week (on July 3rd), the Aussie central bank is expected to hold cash rates at 1.5%. In our stances, the current levels of wage pressures and inflation will likely keep the RBA on hold for some time. The comment concerning the likely direction of the next rates move is not expected to be included in the statement despite some confusion in markets over its omission from the June minutes, but its 'absence' may not mean a lot.

The rankings of currencies on this framework are mostly unchanged this month. A shift has come from CHF, which given recent outperformance has ended up moving up in rank (from third cheapest currency to the fourth cheapest), but nonetheless, valuations are midrange rather than at extremes, thus leaving the currency with two-sided risks.

The cheaper basket continues to be dominated by SEK and GBP in G10, while the richer end of the spectrum still comprises USD, EUR and the Antipodeans. PetroFX in this framework continues to screen near fair value but still appear cheap vs. the Antipodeans (1st chart).

USD continues to grind gotten richer on the framework and is the richest G10 currency on a cross-sectional basis. Nonetheless, it still is 10%pts cheaper than 2016 levels indicating that there continues to be a two-way risk to the currency. Among reserve FX, despite the YTD weakness, USD continues to screen richer than EUR on this framework. Valuations for neither USD nor EUR are at an extreme yet. JPY is now cheaper than EUR, while CHF remains near fair value (2nd chart). Courtesy: GS

FxWirePro launches Absolute Return Managed Program. For more details, visit: