Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

EURCHF is so far tracking our forecast which assumes a softening in the SNB’s intervention regime and a resultant orderly decline of around one cent per quarter in the cross to 1.03 by year-end. The SNB is certainly not about to abandon the franc entirely to market forces -the excess net private sector demand for CHF stands at 10% of GDP, which would likely cause the franc to appreciate by 5-10% in the absence of countervailing FX intervention.

Nevertheless, there is evidence from the central bank’s rhetoric and action that the SNB is becoming more flexible in its currency policy and that the objective is mutating from the maintenance of a stable bilateral exchange rate versus EUR towards controlling the pace of franc appreciation.

Hence, sell USDCHF through a 3-month put spread. Stay short EURCHF

What has Switzerland to do with US FX policy one may ask? The answer is that Switzerland is the third largest holder of FX reserves globally (6% of global reserves for an economy which accounts for 0.9% of global GDP).

It is also one of only two countries that currently exceed the threshold for FX intervention the US Treasury has established as prima facie evidence of currency manipulation (persistent, one-sided intervention exceeding 2% of GDP). Switzerland is also the sixth largest owner of US Treasuries (rising to fourth if offshore centers are excluded).

In short, Switzerland has a long and enduring history of FX intervention. This may be regarded as a legitimate expression of domestic monetary policy by some observers, but could equally be construed as currency manipulation by others.

The simple point is that the international climate has become less permissive towards large-scale intervention and this is a secondary reason to expect the SNB to progressively taper the amount it intervenes. The primary reason is that there is no compelling economic rationale for the SNB to frustrate all of the CHF appreciation that would be justified by Switzerland’s juggernaut current account surplus.

We stay short EURCHF in cash and add downside in USDCHF through a diagonal debit put spread.

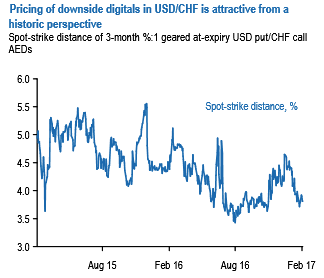

Our choice of a put spread is motivated by: 1) the French election calendar should prevent USD/Europe from running away ahead of the second-round presidential runoff on May 7 and the Assembly elections on June 11 and 18, and 2) digitals are reasonably priced for downside in USDCHF (refer above chart). The digital profile can be replicated with a vanilla spread.

Buy a 1m3m USDCHF debit put spread (with strikes of 1.0225 – 0.9515) (at spot reference 1.0005).

We encourage shorts EURCHF in spot FX as IVs for this pair is conducive for optionality (least IVs among the lot), so, go short for targets up to 1.0525 (almost 100 pips) with a strict stop loss of 1.0755 levels, spot reference: 1.0645 (first entered 1.0720 November 11th).