FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data

FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data  FxWirePro: USD/JPY advances as traders test Japan's intervention resolve

FxWirePro: USD/JPY advances as traders test Japan's intervention resolve  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  FxWirePro: USD/ZAR gains some ground, but downtrend remains

FxWirePro: USD/ZAR gains some ground, but downtrend remains  FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report

FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support  Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro : EUR/NZD slips lower after soft US jobs report

FxWirePro : EUR/NZD slips lower after soft US jobs report

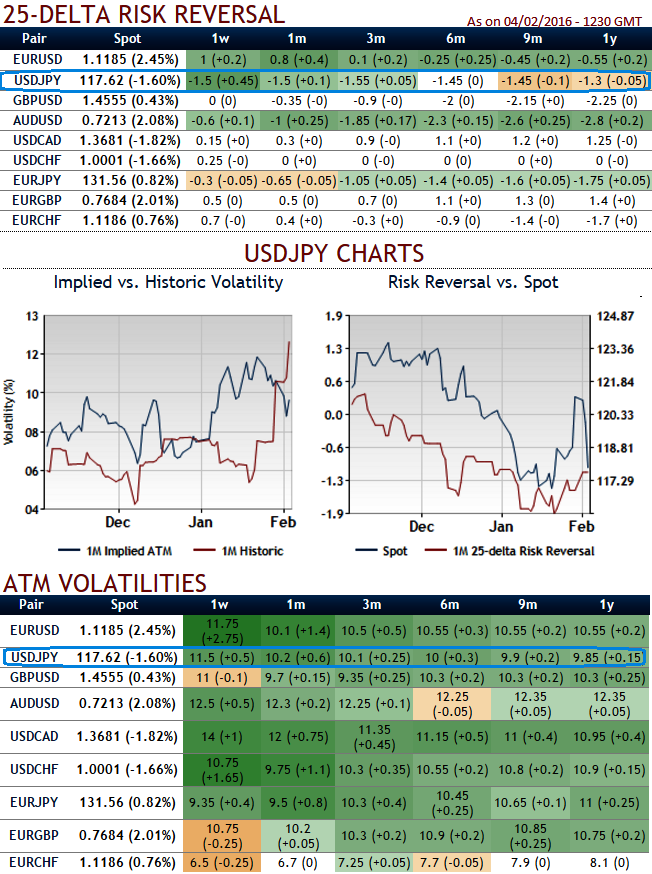

From the recent rate change by BoJ makes commercial banks that park surplus reserves at the central bank to negative 0.1% in a slightly awful stimulated pointing at serving its economy to cushion the potential threats of deflation.

By pushing rates into negative territory, the BOJ is in effect penalizing commercial banks for not lending aggressively by charging the institutions for holding excessive reserves at the central bank.

Soon after the unanticipated monetary policy decision, major central banks in the world have now begun offering rates in negative territory for the first time ever, USDJPY jumping into a serious sell.

The BOJ is currently pumping ¥80 trillion into the Japanese economy ($674 million) through a large-scale quantitative easing program that has achieved varying amounts of success over the last three years.

Please observe how delta risk reversal numbers are consistently spiking higher negative values in a long run (flashing at 1.3 for 1 year expiries). Volatility smiles most frequently show that traders are willing to pay higher implied volatility prices as the strike price grows aggressively out of the money.

Well, the test encounter now is in determining which strikes you should use in this strategy. The broader the strike difference between short and long puts, the fewer puts you need to sell to cover the price of the long puts. But at the same time, the coverage of long-to-short is going to be more difficult in the event of assignment.

The current spot FX is trading at 116.812, we expect dips extending up to 116.084 and even at 115 levels in near terms. So, it is understood that bearish momentum is bolstering as we saw that from delta risk reversal table and technical indications in the previous post. Hence, aggressive bears can initiate strategy using ATM puts.

Unlike a simple naked put, put backspreads have an extra-long that has not only leveraging effects, a short option at a lower strike that caps your reward but also reduces the net cost of the trade. So, the recommendation for now is to add an extra-long on put with 1W expiry to the existing debit put spreads. Instead of 2:1, bears can eye on 3:2 ratio in the spread for leveraging effects.

With these narrow strike differences, the profit potential is greater, so that the ratio needed is also lower to profit on underlying movement. As you can see IVs are reducing in longer duration you would want to take this opportunity to short narrow strikes. On the flip side, if you think this pair can go lower, but not crash below 115.00 (the OTM shorts are recommended). Caution: If you think the pair is going to crash, you should be loading up on put buys in existing strategy. The total cost of the trade is going to be the difference between the prices of the two options.

Since the option you sell will always be lower on the skew curve it means you are getting a better deal on what you are selling compared to what you are buying. It makes this strategy a good one if the skew is running a little hot but USDJPY hasn't rolled over that much.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: USD/JPY OTC indications pile up bearish sentiments, threatening dollar bulls – load up shorts in PRBS on sinking IVs

Friday, February 5, 2016 7:10 AM UTC

Editor's Picks

- Market Data

Most Popular